Music festivals and concert arenas used to be synonymous with summer. But this year, the cancellation of live shows—the music industry’s bread and butter—has closed the gates on a vital revenue stream for many artists. Not everyone is suffering, though. Some have faced the music by selling their song catalogs. But does that work for every artist?

When the Music Dies

Disposing of an asset always involves trade-offs—and selling a song catalog is no different. Before deciding if it makes sense, consider several factors. Chief among them is the catalog’s current value compared to what it might fetch in the future. Unfortunately, artists often find themselves at a distinct disadvantage when ascertaining their catalog’s worth. This makes it difficult to negotiate a price, especially when bargaining with sophisticated counterparties like large media conglomerates or investment firms. To avoid letting it go for a song, artists should arm themselves with the financial knowledge and strategic advice that can help them succeed at the negotiating table. It starts with understanding what drives a catalog’s value.

What’s It Worth to You?

Catalog sales go back many decades—with major artists like The Beatles, Michael Jackson, and David Bowie commanding outsized payments for their songs. Today the prospect for songwriters and producers seems more compelling than ever, due to three main factors:

1. Ease of valuation: Thanks to the data generated by streaming services, calculating the value of a song and projecting its future earnings potential has become more straightforward.

2. Fewer barriers to entry: New technology and globalization have made it easier to be in the copyright management business. New entrants can build their own teams or partner with existing companies to collect royalties around the world. Global administration of copyrights was once a complicated endeavor but there has been a noticeable rise in the number of catalog buyers given the lower barrier of entry.

3. Low-interest rates: Interest rates hover near or below zero in many countries, prompting investors to search for higher returns among nontraditional asset classes whose performance tends to be uncorrelated with equity markets.

Which of these factors counts most for sellers? Interest rates, because of the “time value of money.” In other words, whether the catalog’s revenue will be worth more today or at a future date greatly determines its future overall wealth. The concept lies at the heart of choosing between a lump sum payment or receiving a stream of royalties over a given period.

Today, both inflation and interest rates remain depressed by historical standards, so tomorrow’s dollar will likely be worth almost as much as right now. That means buyers are likelier to pay more for a music catalog than they might otherwise in an environment characterized by higher inflation and interest rates.

Which Scenario Strikes a Chord?

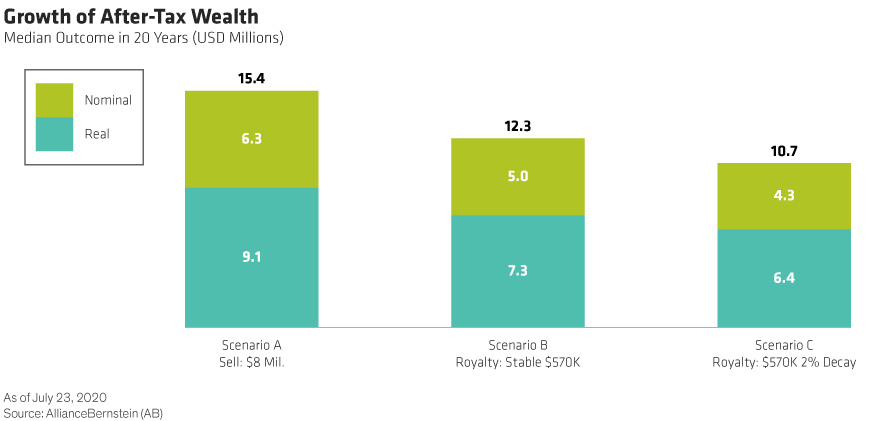

To explore these ideas further, consider Annie, a Tennessee-based artist who’s fine-tuning her choices:

- Scenario A: Sell her catalog today for $8 million and pay capital gains

- Scenario B: Retain a royalty stream of $570,000 per year* and pay annual ordinary income tax

- Scenario C: Same as B, except the royalty stream experiences an annual decay of 2% per year

Annie and her wealth advisor have decided that regardless of scenario, she will reinvest the proceeds in a portfolio consisting of 40% return-seeking/60% risk-mitigating assets.

Which option hits the highest note? We calculate that in 20 years, Annie’s average after-tax wealth will be greatest under scenario A (Display). By selling in the current interest rate environment, she will amass nearly 25% more wealth than with a non-decaying royalty stream. But reduced royalty rates are a reality for some artists. Under those circumstances, Annie would end up with even less wealth—roughly 31% less. The added uncertainty and potential decay of future revenues due to changing consumer preferences, new technology, or reduced royalty rates further propels her towards a lump sum payout.

What Will You Do with the Proceeds?

Even with a compelling sale price, artists also need to contemplate three essential questions:

1. Are the funds earmarked for a planned purchase?

2. Will you invest the money?

3. Who is on your team?

The answers will further inform whether a sale makes sense and how best to deploy the assets. For example, if you answered “yes” to the first question, you probably shouldn’t sell your catalog—unless you plan to diversify your portfolio by investing the proceeds in appreciating assets (see question two) or need capital to repay existing debt.

Note that these questions don’t exist in a vacuum. It’s critical to factor in the tax impact, future capital needs, and other financial implications. A team of professionals—including an attorney, accountant/business manager, and a wealth advisor who are well versed in catalog sales—can help you formulate your goals, assess your opportunities, and execute your wealth plan.

Don’t Let Your Wealth Plan Play Second Fiddle

Before any sale, sit down with your wealth advisor to build a financial plan and investment strategy to develop and implement your wealth goals. Planning for more complex wealth transfer strategies—those designed to pass some of your success on to family or charity, for example—should also be undertaken in advance. Such planning can potentially reduce taxes and minimize the concentration of assets by investing in stocks, bonds, and other alternatives.

While selling your song catalog to supplement income may sound like music to your ears, the intricacies of evaluating its proper worth, when to receive payment, and what to do with the proceeds can be daunting. Planning is the best way to get this right—because unfortunately, you don’t get a second take if you miss your cue.

- Adam Sansiveri

- Senior Managing Director

- Stacie Jacobsen

- National Director—Wealth Strategies Group

*Royalty stream does not increase with inflation