It’s increasingly common for private companies to go public by listing their outstanding shares directly on an exchange rather than through an underwritten initial public offering (IPO). If you own shares eligible for sale through a direct listing, you’re likely to wrestle with several questions about the impact on your financial picture:

- How much should you sell, and at what price?

- What’s the optimal diversification strategy for the proceeds earned from selling shares?

- What will the tax impact be, both in the near term and for your estate?

- Should you retain some shares in anticipation of future price gains?

How Direct Listings Differ from IPOs

In traditional IPOs, employees and other shareholders may have to wait up to 180 days to sell shares. Direct listings, on the other hand, typically allow immediate sales on a company-established listing date, which signals the opening day for trading. Although the exchange will publish a reference price the night before (based on advance buy and sell orders received by its designated market maker), potential sellers do not have any trading history to guide their plans. It’s impossible to know whether the opening price of the stock will end up being near the top, middle, or low end of the trading range for months to come.

Given the complex issues presented by direct listings, it’s imperative for sound financial planning to guide your strategy for selling shares—and to develop a road map well before your liquidity event occurs.

First, Take Stock of Long-Term Plans

Consider the case of Cynthia, a 57-year-old entrepreneur residing in Wyoming with her 59-year-old husband and 24-year-old daughter. Cynthia co-founded a technology company eight years ago, though she has since left the company. Despite parting ways, she’s maintained an ownership stake of 1,042,000 common shares. Following a phase of rapid growth and a financing round at $40 per share, the company has no further need for capital and has announced it will undertake a direct listing.

In discussions with the company and her CPA, Cynthia confirmed that her private shares were eligible for a $10 million capital gains tax exclusion per the Qualified Small Business Stock (QSBS) rules.[1] Under the QSBS program, investors, founders, or employees who are issued stock from a qualified small business can exclude from their federal taxes a portion of the capital gains upon the stock’s sale.

Cynthia’s past successes and wise investing have enabled the couple to build up a $10 million taxable and $2 million tax-deferred liquid portfolio. Now, with a potential liquidity event looming, we engaged in pre-transaction discovery to help them reflect on their priorities going forward. Cynthia decided this will be her last entrepreneurial endeavor and that she and her husband will dedicate the remainder of their lives to volunteering for organizations with which they shared a common purpose. They looked forward to taking annual trips with friends and family as well. The couple needed $500,000 a year to support their lifestyle and volunteer work. They also wanted to ensure they could pass wealth to their daughter in a way that was sensitive to income and estate taxes.

Above all, the couple understood the risk to their family’s future fortune of maintaining a concentrated stock position and wanted to pursue a thoughtful approach to diversifying the proceeds of the direct listing.

Next, Consider How Much You’ll Need

To arrive at a specific selling strategy, we applied our proprietary Wealth Forecasting Model to calculate how much capital the couple would need to secure their lifestyle spending, even throughout potentially hostile market conditions. We call this amount core capital.

Although she had been a high risk-taker as an entrepreneur, when it came to ongoing investments, she and her husband decided they’d be comfortable with a conservative asset allocation. We recommended 20% global equities, 15% alternatives, and 65% fixed income. Based on this allocation, we determined that the couple’s core capital requirement was $30 million, or an additional $18 million above their current liquid investments.

Planning for a Range of Potential Opening Prices

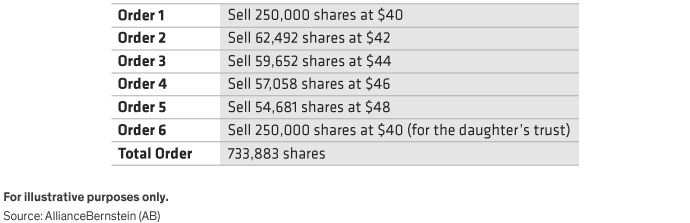

As the technology company’s direct listing approached, we helped the couple develop a further diversification framework. Referencing the tech company’s last round of financing, Cynthia had over $40 million of share value—more than enough to cover the couple’s spending goals. They could consider measures to start providing for their daughter and charity. In partnering with their estate planning attorney, we advised them to immediately establish a non-grantor trust for their daughter and gift 250,000 shares of Cynthia’s QSBS stock to the trust, so it would also be able to exclude up to $10 million in capital gains.

Assuming a range of potential reference opening prices, we calculated the number of shares that could take full advantage of Cynthia’s $10 million QSBS gain exclusion. For the remaining $8 million the couple needed post-tax to reach their core capital, we called for opportunistically selling a decreasing number of shares at higher reference price thresholds, by placing four orders scaled at intervals from $40 to $48.

Our review of past direct listings suggested a strong possibility that the opening trade would be at least 20% higher than the reference price. For example, Coinbase opened at a price 52% higher than its reference; Palantir, 38% higher; and Spotify, 26% higher.

The exchange announced a reference price at $40 (in line with the last funding round), and we entered a tiered set of limit orders:

Modeling the Next 40 Years

The stock opened at $51.50, nearly 30% higher than its reference, so all the orders were executed at that price.

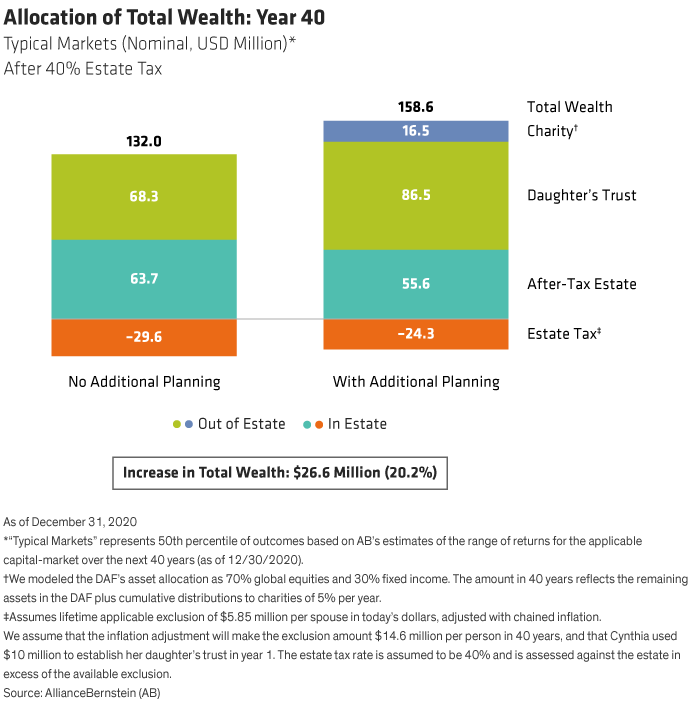

We next applied our model, including single-stock projection tools, to estimate how much money the couple and their daughter’s trust would have at the end of 40 years after spending an inflation-adjusted $500,000 per year and accounting for estate taxes. We modeled the trust’s asset allocation as 75% global equities, 15% alternatives, and 10% fixed income.

We felt comfortable recommending that the couple contribute 100,000 of Cynthia’s shares, with a value of around $5.1 million, to a Donor-Advised Fund (DAF). In a DAF, the shares can be sold without delay in the market. Not only would this provide a tax deduction to reduce their current-year capital gains tax, but the fund could be managed over time to meet a portion of their philanthropic goals.

In addition, we recommended that the couple plan to give away any potential future appreciation in value on 100,000 shares by establishing a series of two-year rolling Grantor Retained Annuity Trusts (GRATs) over the next 10 years, with any gains being transferred to their daughter’s trust.

By adding these strategies, their projected future median wealth values improved considerably. (Display)

The Result: Increased Wealth and Lower Tax Liability

Cynthia and her husband were able to apply a thoughtful diversification strategy in the direct listing that addressed their specific goals. The couple secured their lifestyle spending and started providing for their daughter, taking advantage of two QSBS exclusions. They began to fund their support of charity in a tax-efficient way by establishing a DAF. They also contributed shares to a GRAT strategy that would benefit their daughter should the company’s stock price grow over time. The remaining 108,117 shares (10%) could be used for a range of outcomes:

- donated to the DAF in future years, offsetting any additional gains,

- contributed to the rolling GRAT strategy to further reduce their taxable estate and maximize wealth transfer to their daughter, or

- sold outright to accomplish additional spending goals.

Altogether, by adopting the strategies we recommended, they were able to decrease their estimated estate taxes by $5.3 million and increase their total wealth by $26.6 million, or 20.2%.

If a direct listing opportunity arises, your Bernstein Financial Advisor can recommend a strategy to help you achieve your goals.

- Morgan Campbell

- Associate Director—Wealth Strategies Group

- Richard Weaver

- Senior National Director, Executive Services, Institute for Business Owners and Corporate Executives

1 See IRC Sec. 1202 for the rules surrounding gain exclusion from the sale of Qualified Small Business Stock (QSBS).