Despite the stock market’s strong finish in 2020, not every investor joined the party. According to the Federal Reserve, total assets held in money market funds surged over $1 trillion in the first half of 2020 and now stand at $4.4 trillion.1 Balances swelled for a variety of reasons, including investors cashing in on stock-based compensation like options and grants, but waiting to invest the proceeds.

Investors’ reluctance to move off the sidelines can partly be explained by lofty stock market valuations. But for those with a large, concentrated position in a publicly-traded stock, accumulating cash is often a conscious choice aimed at offsetting risk. Holding cash in this “barbell” approach—designed to couple the low-risk profile of cash with the higher risk of a single stock—sounds appealing. So we put it to the test.

Is Cash Clutch When It Comes to Risk?

Consider an investor in the top federal tax bracket who sold half her company stock following a successful IPO. After paying taxes, she now holds $5 million of company stock and $5 million in her money market account. We evaluated two conservative approaches to deploying the liquid proceeds:

- Scenario A – Keep the funds 100% in cash

- Scenario B – Invest 80% in muni bonds and 20% in globally diversified stocks

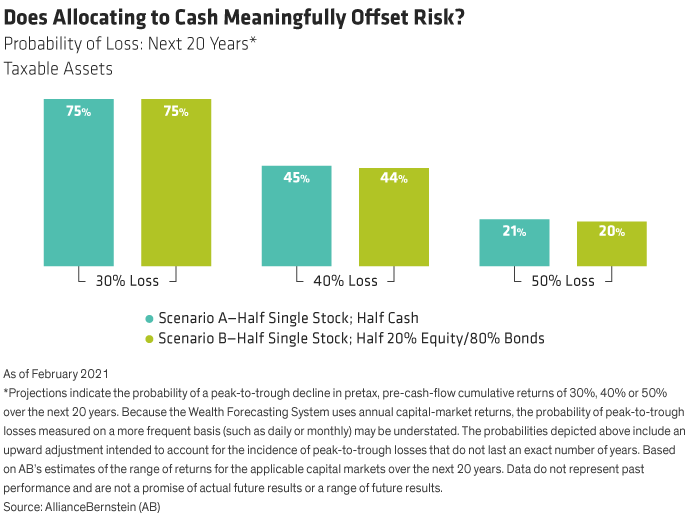

First, let’s gauge the extent to which a heavy single-stock concentration dominates a portfolio’s risk profile. To do so, we modeled the probability of different degrees of losses (30%, 40%, or 50% from peak price to trough)—at some point over the next 20 years—using our two scenarios. The first portfolio was comprised of half single stock and half cash, while the second invested half in single stock and the balance in an 80%/20% mix of muni bonds and global equities (Display).

Cash Fails to Come Through

Surprisingly, changing the allocation for the liquid proceeds makes very little difference. The overwhelming exposure to company stock remains the dominant driver of investment risk, regardless of how the remaining half of the portfolio is allocated. An investor with a portfolio of half cash/half single stock has a 45% chance of experiencing a 40% pull-back at some point over the next two decades. But when the cash is replaced with a conservative mix of stocks and bonds, those odds actually decline slightly. So long as half of the portfolio consists of a single stock, the remaining allocation seems immaterial.

But while risk might be unmoved, return potential is another story. How an investor allocates the liquid proceeds has a huge impact on her opportunity for growth. Revisiting our hypothetical scenarios, an investor in the 50% cash/50% single-stock portfolio could expect it to grow from $10 million to a median value of $13.1 million after 20 years. On the other hand, by replacing cash with 80% bonds/20% stocks, the median value increases by $3.5 million—to $16.6 million (Display).

A More Productive Path for Cash

Clearly, when it comes to single-stock exposure, investors who cling to cash pay a high cost while receiving little downside protection in return. So what should a concentrated investor with idle cash do? First, work with your advisor to determine your strategic asset allocation, balancing your personal risk tolerance with your appetite for growth. Then determine your desired market entry strategy. Keep in mind, you don’t have to go in all at once. There are always trade-offs in investing, but if you are feeling uneasy about entering the markets, consider buying a little at a time.

Finding your footing can be tricky, and our wealth forecasting tools can help. By working with your financial advisor, you can find a clear path to put your cashback to work.

- Christopher Clarkson, CFA

- National Director, Planning | Foundation & Institutional Advisory

- Stacie Jacobsen

- National Director—Wealth Strategies Group

1 Source: Board of Governors of the Federal Reserve System (US)