It’s been a long time since investors have had to worry about inflation. But a strong economic rebound from the pandemic could trigger higher inflation, requiring investors to think about portfolio adjustments and to reconsider some asset classes shunned over the last decade.

People tend to think about the next crisis in terms of past crises. But just like this pandemic-inspired recession isn’t the global financial crisis of 2008, this round of inflation won’t be like the 1970s. While we expect inflation to increase in the short run, we don’t believe it will be the major concern it was 50 years ago. Our expectation is for 2.1% inflation by the end of 2021, trending sideways thereafter.

Still, with global real GDP growth expected to exceed 5% in 2021 and massive fiscal stimulus programs underway, especially in the US, inflation expectations are increasing against an unusual set of market and economic conditions. However, because the recession was short-lived, we believe the supply constraints driving inflation should ease relatively quickly. And as the US economy begins to recover, core inflation should diminish as supply catches up to demand. While some popular measures suggest annualized inflation expectations over the next five years have reached 2.4%, this is still a moderate level, despite being the highest in a decade.

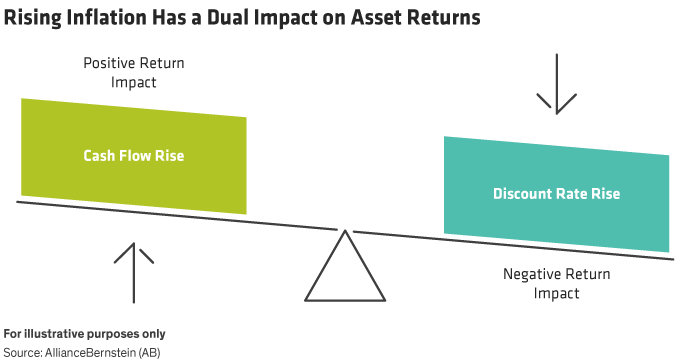

Gauging Inflation Sensitivity for Different Assets

Moderate inflation is both a blessing and a curse. On the one hand, it helps a company’s growth by increasing cash flow. Many companies, especially those that are commodity-related, can pass through higher costs via pricing power, potentially leading to higher margins.

On the other hand, inflation erodes the real value of your investment returns. If inflation leads to higher interest rates—as it often does—it increases the discount rate used to gauge the present value of future cash flows. Higher discount rates cause the market to devalue assets with future cash flows, and the further out they are, the more detrimental the impact. How inflation affects the value of any given asset depends on the net impact of these two phenomena—greater expected cash flows and higher discount rates (Display).

For example, with higher discount rates, stocks of hypergrowth companies valued on earnings expected in 7–10 years might not fare as well as those of value companies with current earnings and lower valuations. And all else equal, shorter-duration and higher-yielding bonds should outperform longer-duration and lower-yielding instruments. In short, some of the investments that have been big winners in recent years may not be in the future if inflation comes back.

Fixed Income Considerations for Inflationary Times

For US Treasury investors, the starting place for inflation today is tough—there’s not enough inflation-adjusted yield to cushion the pain. On a five-year US Treasury yielding 0.84%, the real yield with 2.00% inflation is –1.16%. Negative real yields destroy an investor’s spending power. It’s time to adjust fixed income portfolios to improve your portfolio’s response to inflation. We recommend taking a close look at the vulnerabilities of current fixed-income allocations to inflation.

To start, consider modestly reducing the portfolio’s duration, or sensitivity to interest rates. Shorter-term bond prices fall less as market yields increase. They also can be reinvested in higher yields sooner. But, in the current low-yield environment, sitting in short-term bonds won’t cover the effects of inflation.

Will Inflation-Linked Bonds Protect Investors?

Treasury inflation-protected securities (TIPS) and similar inflation-linked bonds globally will outperform comparable-maturity Treasury bonds if inflation increases more than expected. But they are already trading at negative real yields. And if inflation comes with economic growth, inflation-linked bonds will suffer as real yields rise.

Consider reorienting your portfolio to be more defensive against inflation while still capturing income and yield. For many investors, this can be accomplished by tilting the allocation toward credit. That includes increasing the portfolio’s exposure to high-yield corporates, while also diversifying into other sectors with attractive relative yields and low correlations to government bonds. For example, US credit risk–transfer securities (CRTs) are floating-rate bonds backed by real assets—homes—that often benefit from inflation. Issued by Fannie Mae and Freddie Mac, CRTs offer higher yields in exchange for accepting the default risk of a pool of mortgages. Thanks to the robust US housing market, fundamentals look attractive for CRTs.

Finally, inflation could aid bonds tied to the financial sector. As interest rates rise, so do bank margins, improving banks’ credit profiles. In Europe, for example, bank bondholders have benefited from solid balance sheets and supportive regulatory conditions, and rising rates could further benefit both banks and bondholders.

Rethinking the Equity Portfolio

As with fixed income, this isn’t the time to completely rebuild your equity portfolio. But there are some adjustments worth considering.

Lower and falling rates have disproportionately favored growth over value stocks for over 10 years. Growth stocks valued on earnings and cash flows expected many years in the future have seen their price/earnings multiples expand as rates have fallen. If rates rise, this trend could quickly reverse, especially for hypergrowth companies valued on earnings that haven’t happened yet. In other words, hypergrowth companies are quite susceptible to rising bond yields, even if they have cutting-edge technology and strong sales growth, because their future earnings are then discounted by a higher interest rate. Investors in growth stocks should check that their allocations aren’t too exposed to very expensive companies with weak current earnings power. Growth companies with sustainable business models, consistently high profitability and relatively attractive valuations will be better positioned for an inflationary outbreak.

On the other hand, value stocks could benefit from inflation. As COVID-19 vaccinations are increasingly rolled out and countries make progress in combating the pandemic, we believe investors will gain confidence in the trajectory of the nascent economic recovery. That should help support a recovery of more cyclically exposed value stocks. With global value stocks trading at a record 52% discount to growth stocks at the end of February, we think investors should consider initiating or increasing value exposure in equity allocations.

Defensive equity sectors and low-beta stocks have underperformed during inflationary cycles in the past. Some bond proxies—where investors look for income and stability—such as utilities and consumer staples, are among the cheapest stocks today, so they may be less sensitive to inflation than in the past.

Emerging-market (EM) stocks deserve attention, too, as in fixed income portfolios. Beyond the faster growth in most EM economies, many produce commodities. If the global economy is heating up, commodity prices should too.

Real Assets and Commodities

Investors may want to consider other asset classes that perform well during inflationary periods, including commodities, real estate, foreign exchange and commodity-linked equity investments. Real assets, with their value tied to underlying physical assets, have historically performed well in rising inflation. Real assets tend to be closely linked to economic inputs—labor, capital and materials—and as their prices increase, the value of real assets tends to also rise.

The last decade of loose monetary policy led to inflation in financial asset prices, but not in the economy, so real asset prices suffered. Many real assets are now under owned in portfolios, but the combination of fiscal stimulus––which will support real economic activity––with accommodative monetary policy points to higher inflation. Real assets not only should benefit from this shift, but they’re also attractively valued.

Inflation is very difficult to forecast. We believe a diversified basket of real assets will provide the best risk/return trade-off and inflation defense. This basket should be additive to core positions rather than replacing them, in our view. Not all asset classes or investments will be appropriate for every investor.

There’s no need to fear the specter of inflation. With some prudent adjustments, investors can prepare for a moderately inflationary environment and position portfolios to prosper as the pandemic recovery progresses.

- Ronit Walny

- SVP/Head of Fixed Income Product Management—Global Business Development-Fixed Income-NY

- David Wong

- SVP/Senior Portfolio Manager—Global Business Development-Equities-Hong Kong

- Mark Gleason

- VP/Director, Multi-Asset Product Manager—Global Business Development-Multi-Asset-NY