Last year’s Coronavirus Aid, Relief, and Economic Security Act (CARES Act) provided crucial incentives that encouraged individuals to give to charitable organizations during a time of unprecedented hardship. Today, with the need just as high, the government has extended the tax breaks. Here’s a summary of how you can benefit from The Consolidated Appropriations Act of 2021 (CAA), signed into law on December 27, 2020:

For taxpayers who do not itemize their deductions: The roughly 90%1 of individuals who do not itemize can take an above-the-line deduction. This move directly reduces gross income before taxes—of up to $300 (married couples filing jointly can deduct up to $600)—for cash gifts to certain charitable organizations. But be sure to maintain appropriate records when claiming the deduction; the Act increased the penalty for overstatements from 20% to 50%.

For taxpayers who itemize their deductions: The limitation for qualified cash contributions to specific charities remains at the higher rate of 100% adjusted gross income. Further, it’s increasingly apparent that qualified cash gifts can be “stacked” on top of other gifts that are constrained by normal AGI limitations to offer an even greater benefit.2

For corporations: The new legislation kept the annual deduction limitation for corporate contributions at 25% (increased from 10% by the CARES Act) through 2021.

As was the case in 2020, gifts to Donor-Advised Funds (DAFs), private foundations, and supporting organizations do not qualify for the above-the-line deduction or increased annual limits.

Stacking Deductions While Maximizing Giving

To boost the benefit from the higher annual limits, try these strategies:

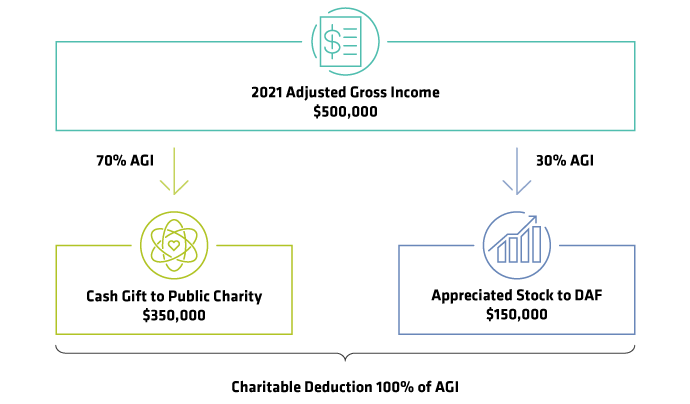

- Give more and use the charitable deduction without hitting AGI thresholds: Consider a donor with an AGI of $500,000 in 2021 (Display). She mapped out a plan to maximize her deduction while giving to charities now and down the road. First, she immediately supported local COVID-19 relief efforts with a $350,000 cash gift to a public charity. She then planned to deploy the second round of donations from her DAF, which she initially funded with long-term appreciated stock. By taking advantage of the temporary tax benefits under the CAA, she receives a combined deduction of 100% of AGI—thus reducing her income taxes—while quickly disbursing funds to preferred causes at a time of heightened need.

- Couple charitable gifts with income-generating strategies: The CAA also offers unusual planning opportunities. For example, donors with stock options may exercise them, make a gift to charity, and take a deduction in the amount of the gift up to 100% of AGI, effectively reducing—or avoiding—the tax cost from exercising.

At the other end of the spectrum, some Americans may have lower taxable income this year due to the pandemic, along with a lower effective tax rate—a situation ripe for a Roth IRA conversion. When combined with the repeal of the AGI limitation on cash gifts to public charities, donors making a large enough donation could convert a portion of their traditional retirement account to a Roth tax-free.

Although these tax incentives offer a significant benefit, donors should weigh them against the advantages of other giving strategies. For example, you may be better off making donations from non-IRA assets—especially when gifting appreciated securities (to avoid capital gains tax exposure)—thereby preserving the IRA’s tax-deferral benefits.

One break the CAA did not extend was waiving required minimum distributions (RMDs) for this year. So unless Congress takes action, unlike last year, RMDs must be made in 2021. Donors may want to consider utilizing a qualified charitable distribution (QCD) to make a charitable gift to offset all or part of the taxable income from their RMDs.

Could Potential Tax Law Changes Impact Charitable Giving?

Given the Democrat’s narrow margin of control in Congress, partisan legislation—including President Biden’s tax proposals—will likely meet heavy scrutiny. But if the tax proposals do gain traction, the attractiveness of charitable giving may change for some. For example, one of the president’s campaign proposals was to raise the top marginal long-term capital gains rate from 23.8% to 43.4% (inclusive of the 3.8% net investment income tax) for taxpayers with income above $1 million. Such a change would make donating appreciated securities to avoid capital gains more compelling for very high earners.

President Biden also proposed capping the value of itemized deductions at 28% of income for those earning more than $400,000. Taxpayers earning above that income threshold would face limited itemized deductions, including the charitable income-tax deduction, thus reducing the value of the deduction for high earners.

Doing Your Part

Unfortunately, changes to tax policy are difficult to predict. Despite this uncertainty, the tax incentives first created by the CARES Act and extended by the CAA remain compelling.

Philanthropy is first and foremost about helping others and the world needs it now more than ever. Donors should focus on their charitable intent—what they want their money to accomplish—and how and where they want to give. Then they should work with professional advisors to optimize their tax benefits—by choosing which assets to give and the timing of their donations. As you’re doing your part to make a difference, it makes sense to maximize the benefits—both for you and your cherished cause.

- Jennifer Ostberg, CFP®, CAP®

- Director—Personal Philanthropy Services

- Robert Dietz, CFA

- National Director, Tax Research—Investment & Wealth Strategies

1IRS reported itemized deductions by only 11.4% of all individual tax returns filed in 2018.

2Section 2205(a)(2)(A)(i) of the CARES Act (Pub. L. 116–136) states that “any qualified contribution shall be allowed as a deduction only to the extent that the aggregate of such contributions does not exceed the excess of the taxpayer’s contribution base (as defined in subparagraph (H) of section 170(b)(1) of such Code) over the amount of all other charitable contributions allowed under section 170(b)(1) of such Code.” Also see “Qualified Contributions” as described in the 2020 Instructions for Schedule A of Form 1040.