Selling a business after years of hard work triggers a flood of emotions for most business owners. The relief, joy, and excitement of seeing the proceeds hit their account is often mixed with anxiety as owners wonder what to do with their newfound cash. Those who deferred planning now face pressing questions, including:

- Will the proceeds be enough to sustain my lifestyle?

- How should I invest the proceeds?

- The market is at an all-time high; is now a good time to invest?

- Should I invest all at once or stage my entry over time?

While answering these questions may seem daunting, the key is to define what happiness looks like and how newly acquired wealth might help fulfill specific life goals.

Mapping the Long Term

To determine how best to deploy the net proceeds, start by quantifying core and surplus capital. Think of core capital as the amount an owner needs today to sustain her lifestyle with a high degree of confidence for the rest of her life. Surplus capital, on the other hand, represents extra wealth that can be used opportunistically to accomplish secondary goals like funding discretionary expenses, or gifts to family or charity.

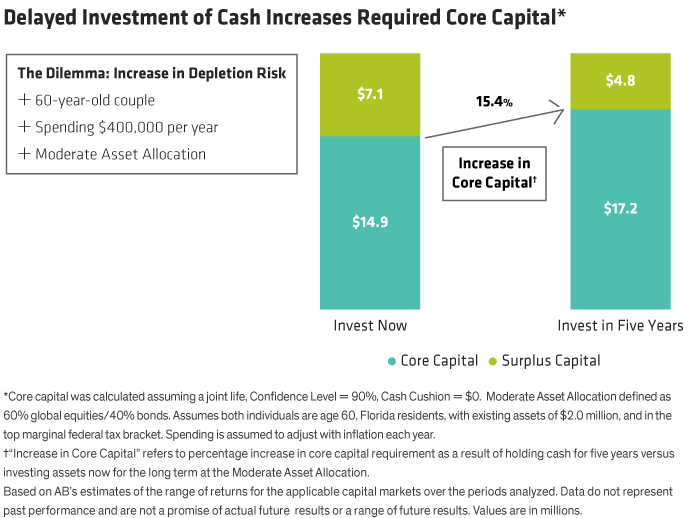

Consider the Cashers, a 60-year-old couple who recently sold their business and received after-tax proceeds of $20 million. The couple wants to maintain their $400k per year in lifestyle spending while assuming only a moderate amount of risk. Using our proprietary Wealth Forecasting System, we quantified their core capital at $14.9 million and their surplus capital at $7.1 million when accounting for their existing assets of $2.0 million. Notably, these figures assumed that all their capital was fully invested.

While the Cashers seemed comfortable with a moderate asset allocation when it came time to put money to work, they hesitated. Will a month or two delay materially affect long-term wealth building? Not likely. But languishing in cash over several years could. For instance, holding cash for five years while waiting to invest increased their core capital by 15.4%—from $14.9 to $17.2 million (Display).

But the Market Is So High!

The Cashers felt torn. They wanted to avoid overfunding their core but also worried about buying in “at the top.” Yet when it comes to investing, there is never a perfect entry point. The market doesn’t send personal invitations—and if it did, some might reject them anyway. Consider the market conditions on March 23, 2020. In retrospect, it was the perfect moment to invest, though the “invest now” sign was obscured by the pandemic’s gloom.

Plus, even if you consistently invested at market highs, you could still generate attractive returns. Since WWII, an investor who bought at each bear market bottom earned 11.5% on average versus 9.6% for an investor who bought at each market top. And while it may feel uncomfortable to plow ahead at the peak, it’s not unusual. Since the market has historically trended higher, it has ended up trading near its all-time high roughly 43% of the time.

Take the Plunge or Wade Slowly Over Time?

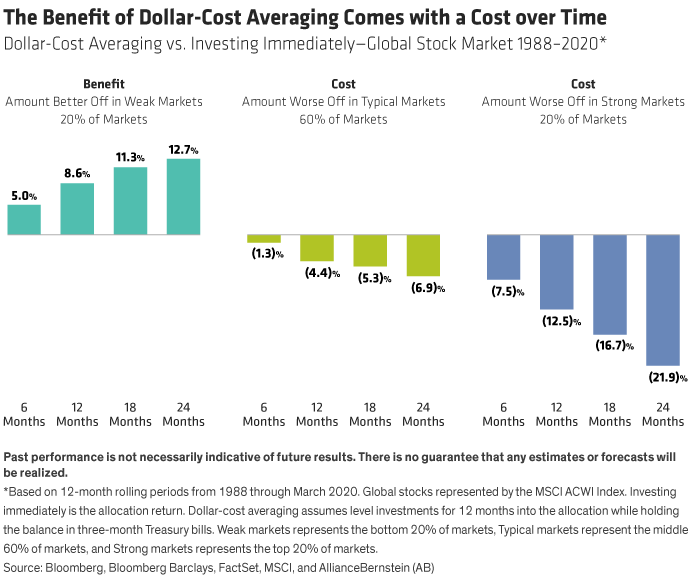

Framing the historical context comforted the Cashers, though they remained reluctant to fully commit—a common sentiment among business owners. Successful entrepreneurs are usually innate risk-takers when it comes to their own ventures because they feel they’re in control. In contrast, markets seem irrational at times. Many business owners fear watching wealth they’ve spent decades building dissipate just because they’ve invested at an inopportune time. To combat this, some prefer to slowly dip their toes in the water by investing a little bit at a time—an approach called dollar-cost averaging (DCA).

Given that markets tend to drift higher over the long haul, DCA generally yields less wealth than going all in. Our analysis shows that the investor who dollar-cost averaged over six months into a global stock portfolio underperformed by 1.3% in typical markets and 7.5% in strong markets compared to investing immediately. Yet DCA can serve as a hedge in deteriorating scenarios. In weak markets, the investor who dollar-cost averaged was 5.0% better off. The Cashers acknowledged this cost-benefit trade-off but still felt more comfortable pursuing a staged entry. Now they wondered how to proceed.

When implementing DCA, time proved the most critical factor. Beyond six months, the marginal benefit that a dollar-cost averaging strategy could provide in weak markets is outweighed by the cost in strong months (Display). For this reason, the Casher’s financial advisor recommended that the couple stage their entry over a three- to six-month period.

Bucketing Your Cash to Achieve Your Goals

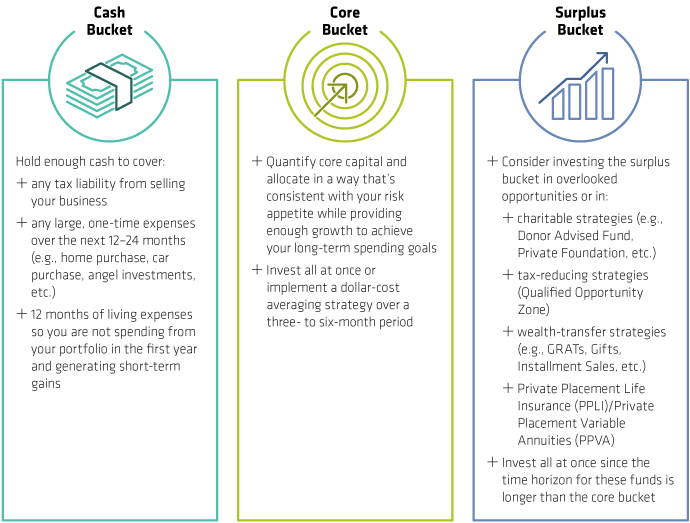

One common mistake that owners make is investing the proceeds as a single pot of money with a uniform focus and allocation. Instead, consider disaggregating your newfound wealth into different buckets with distinct allocations that match time horizons to specific goals (Display).

Business owners who successfully exit often find that their windfall doesn’t come worry-free. Investing a large sum can feel nerve-racking. As you deploy your cash, explore the road map we’ve laid out. In addition to allocating across traditional stock and bond portfolios, consider alternative investments. Although “alts” are frequently illiquid in nature, in the right circumstances they may be an attractive diversifier, and they often have a capital call structure that simulates dollar-cost averaging into the portfolio. While cash can be a conundrum, your Bernstein financial advisor can help you navigate the key planning and investment decisions at each juncture along the way.

- Andrew Bishop, CFA

- Director—Wealth Strategies Group

- Richard Weaver

- Senior National Director, Executive Services, Institute for Business Owners and Corporate Executives