With the odds of experiencing unusually high inflation greater than it’s been in many years, many organizations find themselves reckoning with a long-forgotten foe. Over the near term, we believe the current wave of price pressures—a byproduct of today’s sharp economic recovery, an ongoing boom in goods demand, and supply chain constraints—will likely ease as the economy normalizes. But there’s no guaranteed path for inflation. Astute investment committees should think through the potential challenges, assess their organization’s sensitivity, and proactively position for a potential spike.

Why Does Inflation Matter?

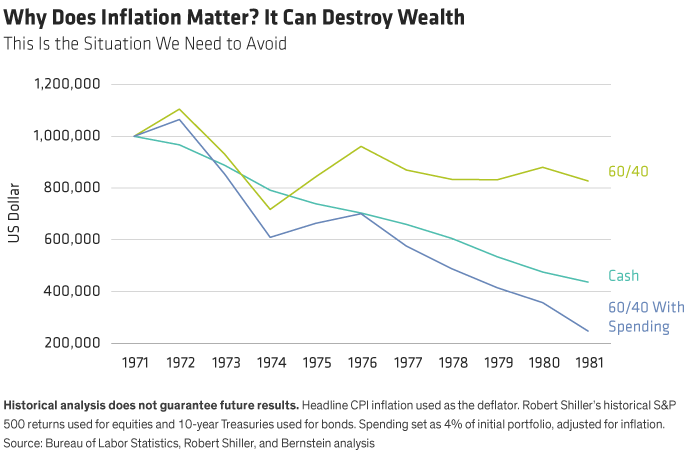

Failing to guard against inflation can lead to disastrous consequences. Consider the inflationary 1970s. If you had $1 million in cash sitting in a safe from the end of 1971 through the end of 1981, you would have lost more than half of your purchasing power. If you had that $1 million in a 60/40 portfolio of stocks and bonds, you would have enjoyed more protection, but would still have lost almost 20% of your portfolio’s real (after-inflation) value. Now consider an organization with no incoming revenue spending 4% of its portfolio’s initial value—with that spending rising with inflation. By the end of those ten years, the organization would have been left with only 25% of its purchasing power.

How can portfolios be protected from what may lie ahead, and which organizations might be at greatest risk?

Portfolio Protection: Smallest Institutions May Be Most Vulnerable

If inflation does break out, stock and bond returns are likely to be poor relative to their normalized history. As a result, investors who are more sensitive to inflation should incorporate some form of portfolio protection. Yet that protection comes with trade-offs—some in the form of volatility, some in performance during disinflationary periods, and some in performance in weaker economic environments.

By adding a balanced package of stocks with pricing power, inflation-protected bonds or inflation swaps, real assets like commodity futures, commodity-linked stocks, real estate and infrastructure, as well as private investments or other assets, investors can substantially improve their performance in what would otherwise be hostile markets while creating more robust, resilient portfolios.

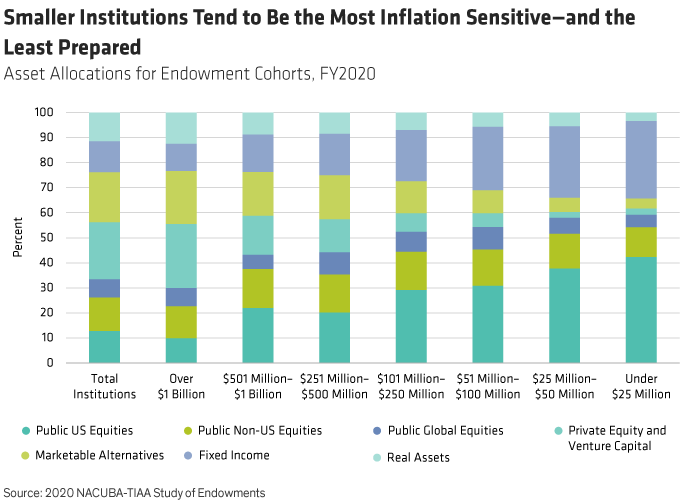

Incorporating an inflation hedge may be particularly important for smaller institutions. Data suggests an inverse relationship between a nonprofit’s size and level of inflation protection in the organization’s investments (Display). For instance, institutions with $1B+ allocated 12.3% to real assets on average, coupled with 21.1% in marketable alternatives. Yet this exposure scales down commensurately with portfolio size. For institutions with assets under $25 million, real assets declined to 3.3% and marketable alternatives stood at just 4%. At the same time, investments in traditional fixed income increased. Taken together, smaller organizations’ positioning reflects greater inflation sensitivity and the least amount of preparedness for an inflationary environment.

Do You Need Inflation Protection? If So, Where?

Given the level of uncertainty—and the trade-offs associated with inflation protection—how can you tell if your institution’s portfolio needs inflation protection? Inflation sensitivity for foundations and nonprofits comes down to three primary factors:

- Risk tolerance and asset allocation

- Spending patterns

- Revenue flows

In many cases, certain asset pools may be prime candidates for inflation sensitive assets, whereas others may not (Display).

Your institution’s risk tolerance and the amount of portfolio volatility deemed tolerable impacts the balance between stocks, bonds, and other assets. For instance, bonds offer a fixed return, which limits their ability to protect purchasing power in inflationary periods. So, a low risk tolerance that leads to commensurately higher bond exposure results in a higher sensitivity to inflation.

Spending is another critical driver. The more your foundation or nonprofit spends, the higher the chance of depleting capital in hostile investment markets. Because inflation tends to be a common driver of unsatisfactory investment returns, protecting against them can extend the runway before you deplete your capital based on your spending pattern.

Finally, the amount of revenue coming in the door—and the growth rate and expected longevity of those flows—also plays a role. Contributions and other sources of capital can be episodic. But in general, the further out an organization can reasonably expect flows to remain positive, the better its odds to keep pace with or beat inflation.

Other factors may also affect your inflation sensitivity. For instance, if the organization owns real estate or other “real” assets, that may lower your inflation sensitivity. Likewise, while we focus primarily on assets, your liabilities also matter—institutions with outstanding loans could also benefit in an inflationary environment if they’re set at a fixed rate and a long term. Your other expenses matter, too. While we focus on inflation broadly, each institution faces a slightly different form of inflation based on the goods and services it purchases. For example, wage and benefit costs for employees in sectors like healthcare have historically outpaced broader inflation and may continue to do so in the future.

Your institution’s exact sensitivity depends on a host of factors, but here are some guiding principles:

Low/No Revenue

- For bond-heavy investors (regardless of spending %), inflation protection is recommended—it can mean the difference between depleting capital or not.

- For equity-heavy investors with high spending, inflation protection is likely helpful…but spending may still need to be cut to reduce the risk of depleting capital.

- For equity heavy investors with low spending, inflation protection is less critical but likely modestly helpful over time.

- For short horizon investors (<10 years) inflation protection is less critical.

Incoming Revenue

- For bond-heavy investors with high spending, inflation protection can substantially boost the probability of sustaining expenses and improve the experience in hostile markets.

- For equity heavy investors with high spending, inflation protection is less critical but could still have a meaningful impact on sustaining expenses in the event of hostile markets.

- For bond heavy investors with low spending, inflation protection can improve the probability of sustaining expenses while also mitigating volatility.

- For equity heavy investors with low spending, inflation protection is less critical.

Inflation Can Be Rare But Consequential

Inflation remains incredibly hard to predict—financial models can capture some elements, but none seem to capture the whole picture. The future can take many different paths and for rare but consequential events like inflation, getting ready for them even if they don’t come to pass can still be the right decision. With the above framework, your institution can adopt a thoughtful and strategic approach to effectively prepare.

- Clare Golla

- National Managing Director—Philanthropic Services

- Greg Young, CFA

- Senior Investment Strategist