As the global economy climbs its way out of the pandemic-induced downturn, mobility is generally improving, demand for goods and services is increasing, and the fiscal policy spigot is wide open—joined at the hip with accommodative monetary policy. And investors are reassessing their portfolios to determine what adjustments are needed in a reshaped landscape.

One risk on investors’ minds hasn’t been much of a factor in nearly a decade: inflation. Price levels have been rising in the US, as rising demand strains the supply of goods and labor. We think this pressure will dissipate later this year, but inflation expectations have risen. And over the longer term, we believe a secular shift is under way—including peaking globalization, resurgent populism and rising government debt—that will exert upward pressure on inflation globally in the decades ahead.

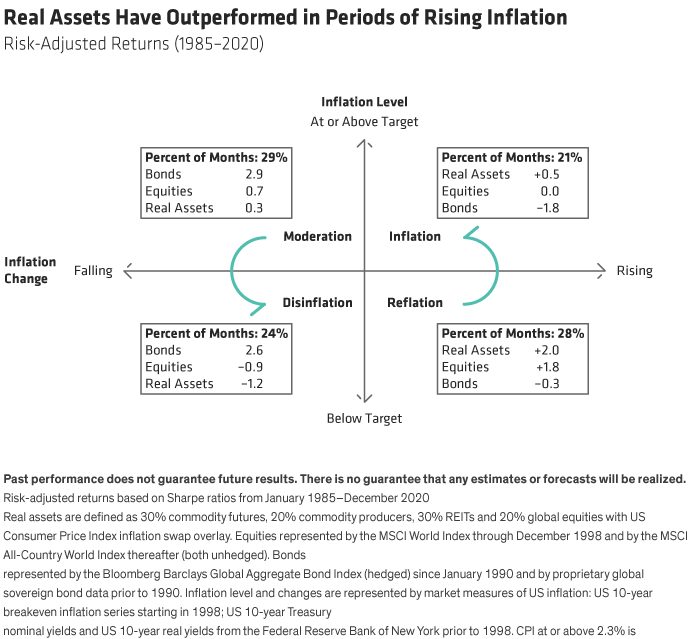

Real Assets’ Inflation-Fighting Credentials

It doesn’t take 1970s-style double-digit inflation to make inflation bite: even modest changes in the inflation regime can erode purchasing power over time. Traditional stock and bond exposures—duration in particular—have faced headwinds in these scenarios. Active management and global diversification across different market segments can bolster equity and fixed income exposures, but we also believe that a strategic real asset allocation will be crucial in defending portfolios.

Historically, diversified exposure to real assets has been effective in months when inflation is rising (Display), including when inflation is also at or above the Fed’s targeted rate. So, in addition to dynamically adapting equity and fixed-income exposures to help ward off inflation’s bite, it seems sensible to consider adding or rebuilding exposure to real assets.

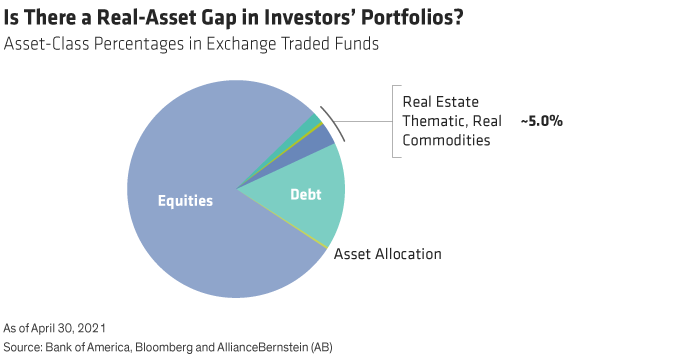

A Missing Piece in Portfolio Inflation Protection

Based on our research, the real-asset hole in allocations is likely sizable. It’s hard to blame investors for neglecting real-asset exposure. With inflation at bay for most of a decade, real assets have languished: their rolling five-year annualized returns have trailed those of global stocks since the global financial crisis. By the end of 2020, despite real assets regaining some ground, the return deficit was –6.8%.

The weak showing by real assets and the lack of a pressing inflation problem has caused exposures to shrivel (Display): the percentage of exchange-traded funds (ETFs) with allocations to liquid real assets is about 5% today. Generally speaking, investors haven’t transitioned to passive real-asset exposure as they have in other asset classes. As a result, most investors likely have a fairly small share of real assets in their portfolios—and many may have none at all.

No Silver Bullets in the Inflation-Fighting Arsenal

Given the dearth of real assets in portfolios, we think it’s an opportune time for investors to assess their portfolio design, adding or boosting exposure as needed. But zeroing in on one real-asset type is too narrow an approach, in our view. Every inflation regime is different: what worked in the past doesn’t necessarily work today—and won’t always work in the future.

Just look at the experience so far in 2021, when inflation and expectations have climbed. Over the past six months, some commodity types have exploded in value—notably energy, industrial metals and grains. The S&P 500 Energy Sector Index is up 45.5% and the S&P 500 Metals & Mining Sector Index is up 59.8%. Gold, on the other hand, has been sluggish, returning 7.6% as measured by the SPDR Gold Shares ETF—failing to offer much of an inflation hedge at all.

It’s a case in point for not being insular in a real-asset strategy.

Diversified, Flexible Real-Asset Exposure Is Key

Actually, when evaluated on multiple dimensions—inflation sensitivity, reliability and cost-effectiveness—no single real asset is a perfect inflation-fighting tool. Gold’s lackluster behavior highlights its low reliability—despite its high inflation beta. It also isn’t very cost-effective based on risk-adjusted return. Real estate equities are much more cost-effective and more reliable, but they’re also less inflation sensitive.

We think a better approach is a diversified real-asset strategy: a blend of real estate equities, natural-resources stocks, commodity futures, gold and inflation-sensitive equities likely to withstand cost pressures better than their industry peers. Throw in flexibility to adapt to changing conditions and tilt toward more effective tools based on the environment, and we think investors have a solution that can fill the real-asset hole in their portfolios.

- Vinod Chathlani

- Portfolio Manager—Multi-Asset Solutions

- Mark Gleason

- VP/Director, Multi-Asset Product Manager—Global Business Development-Multi-Asset-NY