Inflation is challenging for investors for several key reasons. First, it’s incredibly hard to predict beyond the short term as most economic models offer only a glimpse of the puzzle without capturing the full picture. Second, despite inflation itself making rare appearances, inflation protection must remain ever-present—a demoralizing effort when it’s not paying off. Third, different inflation hedges introduce different portfolio risks—some may lower returns, some may increase volatility, and some may not be reliable during inflationary episodes.

Overall, we find a blend of different inflation-sensitive assets works best. But what determines whether inflation protection proves worthwhile? In large part, that boils down to an investor’s inherent inflation sensitivity.

Our analysis suggests that investors who are highly inflation-sensitive can benefit substantially from protection. Investors who are less so may still benefit, but they have more leeway in their decision and the cost-benefit becomes less clear-cut.

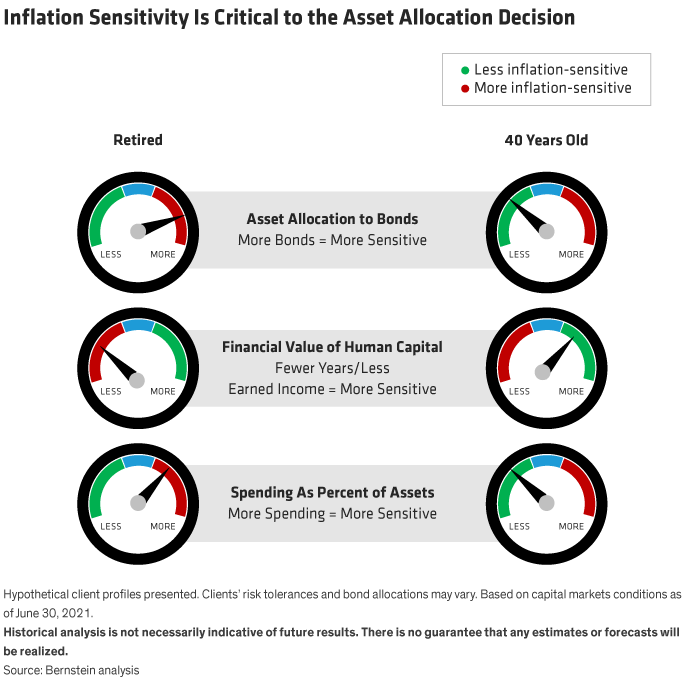

Assessing Your Inflation Sensitivity

So how do you know if you’re highly inflation-sensitive? Primarily, it’s a function of your risk tolerance, and more directly—the mix of bonds versus equities you hold. It also depends on the amount of human capital you can convert into financial capital over time (i.e., whether you’re working versus retired). Finally, the decision hinges on your planned spending rate (Display).

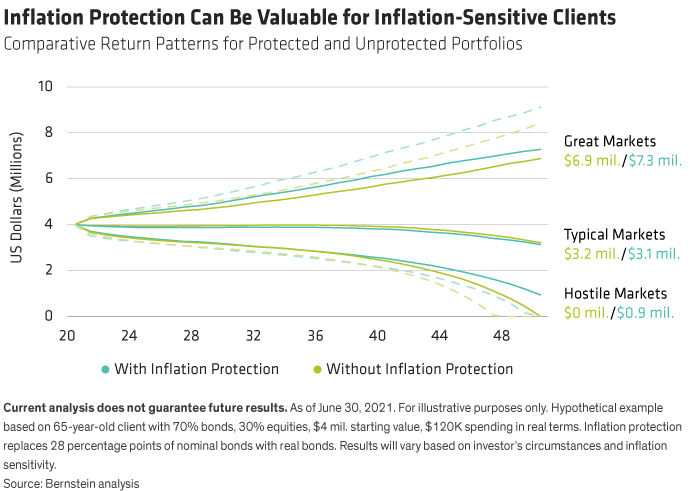

Consider a highly inflation-sensitive investor. In this case, let’s look at the potential portfolio outcomes for a retired 65-year-old with 70% of her portfolio in bonds and 30% in stocks. She’s currently spending 3% of her portfolio per year and aims to maintain that rate after inflation through retirement.

Inflation protection benefits this investor enormously. Utilizing Bernstein’s Wealth Forecasting System, which analyzes the performance of portfolios under 10,000 simulated future paths based on varying economic and market conditions, we can see how she might fare over the next 30 years until she reaches age 95 (Display).

The most striking finding? If she faces hostile markets1 without shielding her portfolio from inflation, she will run out of money by age 95.

This makes sense. Inflation is a leading cause of hostile market environments, hurting the returns of both stocks and bonds while undermining their diversification benefits. By adding inflation protection, we’d expect to buffer the blow and improve portfolio performance during these difficult stretches.

Less intuitively, it’s not just the bottom end of the range where she sees benefits—her performance improves at the top of the spectrum as well. That’s because our investor secures those substantial benefits in inflationary times without sacrificing too much in non-inflationary times. This combination means that her performance is likely to be better overall—she hasn’t just cut off poor outcomes, she’s shifted up her entire range of potential future returns.

Ultimately, this cost-benefit analysis leads to a clear conclusion—highly inflation-sensitive investors are substantially better off with inflation protection.

The Other End of the Field

What about an investor who is less inflation-sensitive, though? How do they fare with and without protection?

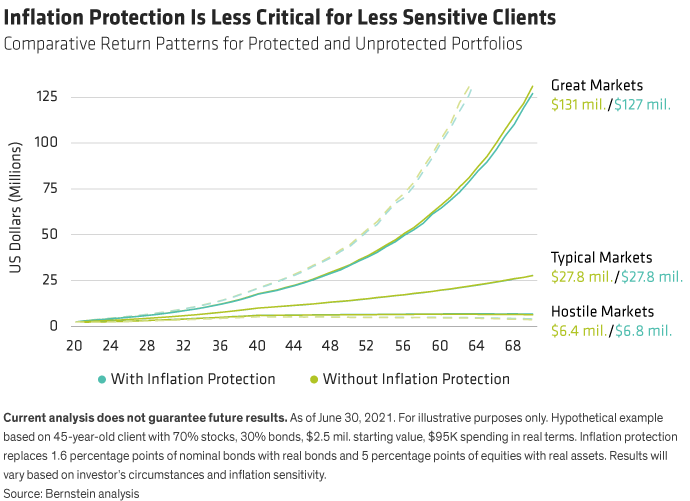

Here, we’ll head to the other extreme by considering a 45-year-old investor and flipping his asset weighting to 70% stocks and 30% bonds. This requires looking ahead 50 years (instead of 30) in order to compare “apples to apples” outcomes at age 95. Essentially, our analysis shows there’s still some benefit in hostile markets, but it’s less pronounced (Display). As with our 65-year-old, there’s relatively minimal cost in a median return environment, although there’s some upside sacrificed in great markets this time.

We also weigh the probability of being able to sustain spending over the horizon, the likelihood of ending with the same or higher principal value, and the chances of suffering a 20% loss. For each, there’s almost no improvement, but also no degradation.

Arguably, this investor benefits marginally from inflation protection. But it’s also understandable if he chooses to forego it. For instance, he could decide it’s not worth the hassle along the way or the regret if sustained inflation fails to emerge. Or, he could consider these marginal benefits overstated due to inflation having a lower probability or protection delivering a reduced payoff compared to what our analysis forecasts.

What About Me?

What if you’re neither 45 nor 65 or your portfolio isn’t 70/30 or 30/70? What might your inflation sensitivity look like?

First and foremost, asset allocation is paramount. If you’re younger and have a lot of earned income ahead of you but are still overweight bonds, you’ll look more like the inflation-sensitive retiree. That means your cost-benefit skews toward securing protection. Or if you’re older and in retirement but still have considerable stock exposure, you’ll look more like the 45-year-old, though you’ll still see a bit more benefit.

Next, the more you spend, the more compelling it becomes to insure against hostile markets. Poor outcomes tend to occur when you combine hostile markets—frequently fueled by inflation—with heavy spending. For those who can, curbing planned spending could prove beneficial. But adding inflation protection may be lower-hanging fruit for those who are locked into their spending patterns.

Your time horizon also plays a role. Counterintuitively, those with a short time horizon (i.e., less than 10 years) are likely to be less inflation-sensitive than it might seem on the surface. For instance, if you’re fortunate enough to be a centenarian, there may be less time for inflation to manifest in the economy and for an inflation hedge to pay off.

Finally, we’ve focused primarily on the assets in your investment portfolio, but other unique circumstances factor in, too. Take real estate, for example. We wouldn’t necessarily count on your personal residence serving as a hedge because local markets are so idiosyncratic. But, if you have large and diversified real estate holdings outside your portfolio, that can make you less vulnerable. Or, consider your liabilities. Those with substantial debts set at a fixed rate for a long period—such as a 30-year fixed-rate mortgage—may also experience lower sensitivity.

Time to Act

When assessing your sensitivity, your financial advisor can serve as a helpful sounding board. Your advisor can also help you explore the merits of inflation protection in the context of your overall portfolio.

When considering what type of inflation protection to add, we’ve noted in our white paper that a blended approach works best. The most robust and resilient hedge is likely to consist of a mix of inflation-protected bonds or inflation swap agreements, stocks with pricing power, and real assets like commodity futures, real estate (particularly equity or floating-rate debt), infrastructure, and commodity-linked stocks. With a balanced approach, investors can expect to navigate whatever the economy and markets throw our way.

- Matthew D. Palazzolo

- Senior National Director, Investment Insights—Investment Strategy Group

- Christopher Brigham

- Senior Research Analyst—Investment Strategy Group

1 Great markets are defined as the 90th percentile of ending portfolio values, typical markets are the median, and hostile markets are the 10th percentile. We also show the 5th and 95th percentiles here for additional context.