In today’s environment, deferred compensation plans seem like a slam dunk. Companies have one more tool to recruit and retain talent in an increasingly tight labor market while their high-earning employees benefit from an additional chance to build savings.

In fact, for many high-income taxpayers, deferring future salary and bonus income into a non-taxable account has become somewhat of an imperative. Strategies like 401(k) plans allow participants to defer $19,500 (under age 50) and $26,000 (age 50 and above) a year. Other plans allow for more deferral, but there are limits under ERISA.

That’s where discretionary strategies, such as Nonqualified Deferred Compensation (NQDC) plans, come in. They allow high-earning employees to defer even more income, often with no caps on how much participants can contribute. This flexibility could help explain why roughly two-thirds of eligible employees participated in nonqualified deferred compensation plans in 2020 versus nearly 54% in 2018, according to the Plan Sponsor Council of America.

What’s the Catch?

NQDC plans offer compelling benefits, but they’re not without risk. For instance, they’re not protected from the company’s creditors in the same way that qualified plans are. If the sponsoring organization goes bankrupt, both plan participants and the company’s creditors can lay claim to the plan assets. And for concerned executives, there’s little margin for error. Rules even prohibit the removal of assets from the plan in anticipation of bankruptcy.1

How should participants size up this credit risk? Look to the company’s rating. Over the last 50 years, the probability of default for an “investment grade” rated company (Aaa to Baa) over a five-year period stood at less than 1.3%. Even for B-rated employers, the probability of default was just 15.54%. But from there, risk increases sharply, with the default risk for Ca-C rated enterprises more than doubling to 39.17%.2

Does Deferral Still Pay Off?

Assuming your company boasts a high rating, what is the benefit of deferring income in a nonqualified plan?

For starters, there is no required minimum distribution. And you can choose how you’d like to receive future payouts—such as a lump sum or in annual installments.3 Plus, with no statutory limit on the amount you can contribute, you could theoretically defer up to 100% of your salary on a pretax basis. This could materially lower your current taxable income. But will some eligible employees sit out if they’ll be deferring into a potentially higher tax environment?

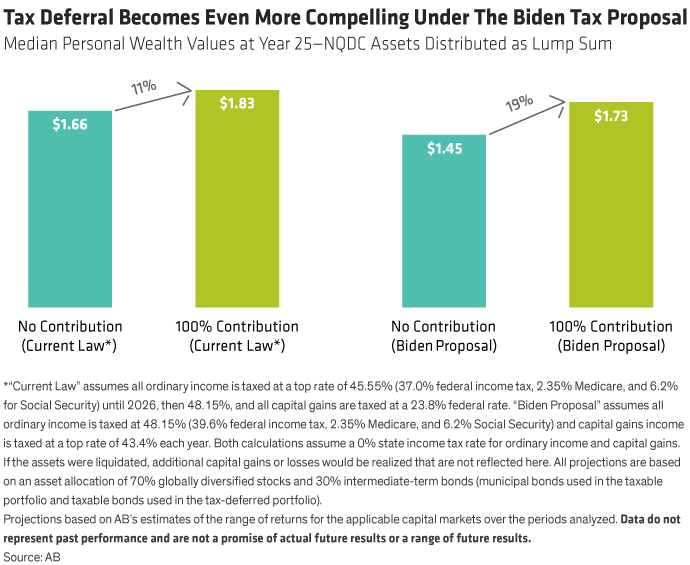

Consider Joaquin and Maria Alvarez, a 40-year-old couple subject to top marginal federal tax rates who are eligible to participate in a NQDC plan. To illustrate the tax-deferral impact under current tax law, let’s assume Maria plans to continue working another 15 years as a pharmaceutical company executive, at which point she’d like to retire.

Maria has been deferring her salary and income in the firm’s qualified plans, but the couple would like to explore the incremental benefit of deferring another $100,000 pretax per year. As a baseline, we found that by simply investing (rather than deferring) the post-tax amount of $54,4504 in a diversified portfolio for the remainder of her working years, Maria and her husband could expect to amass $1.66 million in total personal wealth. But if they had contributed the $100,000 to the NQDC plan instead—and then invested their lump sum payout at retirement—their total personal wealth at age 65 would be 11% greater, or $1.83 million.

How might the situation change under a higher tax regime? Recall that the Biden plan contemplates increasing the federal capital gain rate for taxpayers with income over $1 million to 43.4% (including 3.8% Net Investment Income Tax). In addition, under the proposal the top ordinary income tax rate would increase from 37% to 39.6% for individual taxpayers with income above $452,700 and couples filing jointly with income over $509,300. The upshot? If signed into law, the benefit of tax deferral for Maria and Joaquin becomes even more pronounced at 19% (Display).5

Kicking the Can Even Further Down the Road

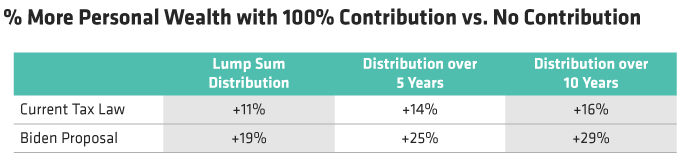

While the benefits of deferral are clear and compelling, they grow even more valuable over time. For instance, if their NQDC plan gave them the latitude to take distributions in equal installments over five or 10 years post-retirement, the couple’s wealth could grow even more.

With tax hikes likely in the offing, finding ways to lower your taxable income could prove worthwhile. If you’re eligible to participate in a NQDC plan, speak to your Bernstein Financial Advisor. He or she can help you carefully review the plan’s provisions, weigh the trade-offs given your personal situation (e.g., time horizon, asset allocation/expected investment return), and gauge your company’s credit risk.

- Austin Cooke

- Vice President—Wealth Strategies Group

- Elizabeth Sohmer, CFA

- Director—Institute for Executives and Business Owners

- Richard Weaver

- Senior National Director, Executive Services—Wealth Strategies Group

1IRC §409A “anti-acceleration” rule.

2Source: Moody’s Investors Services, Default Trends – Global (as of January 28, 2021).

3Under certain conditions, an election change is permitted, but only if made at least one year prior to the date the payment was originally scheduled to begin. Further, a subsequent election would require the participant to defer distributions for at least five years.

4Post-tax amount of $54,450 assumes $100,000, less 37% for federal taxes, 2.35% for Medicare, and 6.2% for Social Security. The 37% rate applies only through 2025. Beginning in 2026, the federal tax rate is assumed to revert to 39.6%. As such, the post-tax amount would be $51,850 beginning in that year and continuing for the duration of Maria’s working years.

5This scenario assumes a post-tax amount of $51,850 for the duration of Maria’s working years.