A thorny issue for investors, inflation has recently captured people’s attention as prices in the US have risen at their fastest pace since the 1980s.

“How big of a risk is the national debt? Is the Federal Reserve behind the curve? Should I overhaul my portfolio to reposition for an inflationary future?” We’ve heard these and other versions of the same question—essentially, what’s the outlook for inflation and how should investors incorporate it into their portfolio—and addressed them in depth in our recent white paper, Inflation: A Clear and Present Danger?

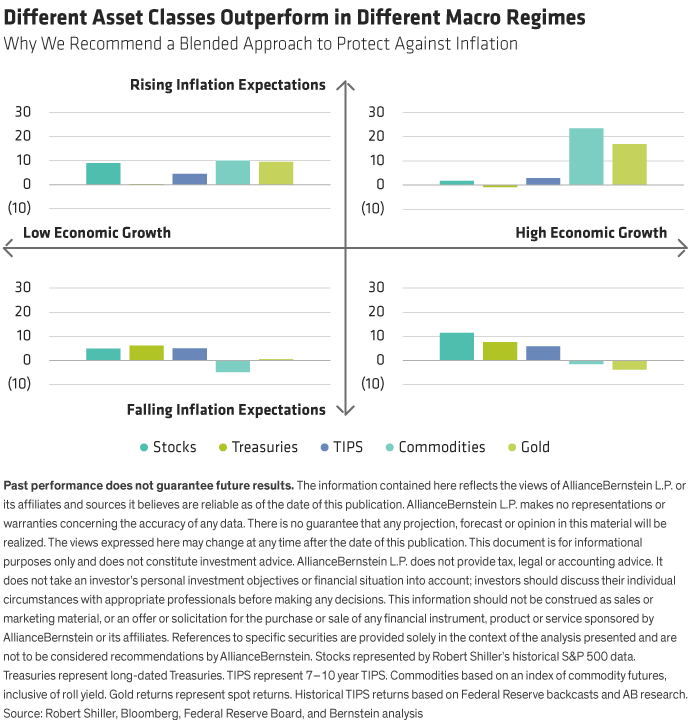

Inflation can be detrimental for investors, harming them in two ways. First, it can impair their purchasing power, reducing the future value of their assets. Second, it can drive poor portfolio performance as it simultaneously damages their returns across a host of asset classes and limits the benefits of a diversified portfolio (Display).

Just as perniciously, inflation can strike without warning—or not strike despite deafening warnings. The challenges are two-fold—determining when it may be coming and protecting your portfolio when warning lights are flashing. Economics offers little certainty. A variety of economic models aim to gauge inflationary risks, yet none paints a complete picture, making forecasts more than a few quarters in advance unreliable and ineffective. Furthermore, these models are often hijacked and used to backfill ideological arguments rather than serving as the foundations of economic analysis and forecasting.

Parsing a Range of Inflationary Paths

As a result of so much uncertainty, we urge investors to consider the full range of possible economic paths and what might propel us down one versus another. Depending on the course of events—and political decisions unfolding in the coming years (not just in the US but also around the world)—plausible paths exist for everything from continued disinflation to runaway inflation. Investors must prepare their portfolios for whatever the economic winds bring.

Part of the challenge? Inflation remains a rare, yet severe event. For those who are sensitive to inflation and at risk if it arises, the wisest course is to pay what’s effectively an insurance premium to protect against it. Yet, because it’s rare, the odds are high that these same investors will look back and—when inflation fails to materialize—regard that insurance policy as money ill spent. We believe investors need to make the best decision they can with the information at hand and focus on the quality of the decision over the eventual outcome.

Who Needs Protection?

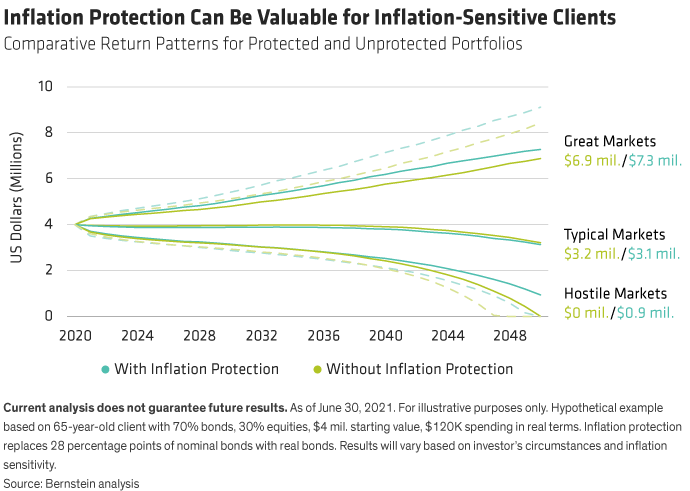

Our analysis concludes that most, if not all, investors are at least as well off with inflation protection as they would be without it. For investors who are extremely sensitive to inflation, the cost-benefit lies squarely on the side of protection. While some investors can likely get by without protection over time, for highly sensitive investors, that hedge can be critical to their financial future (Display).

What drives inflation sensitivity? The most important determinant is your asset allocation, which flows from your risk tolerance. If you have a low risk tolerance and a high bond allocation as a result, you’re going to be more sensitive to inflation. Two other critical determinants are the amount of human capital you can convert to financial capital over the course of your career as well as your current and future spending levels relative to your assets. The fewer years of work you have remaining or the lower your income during that time, the more sensitive you’ll be to inflation. Likewise, the more you plan to spend over the remainder of your lifetime, the more exposed you are to hostile market environments, which can arise due to inflation. In addition, other unique circumstances like real estate holdings, mortgages, or other debt can affect your inflation sensitivity.

What Lies in Store?

Of course, the question we hear most pertains to our outlook. In short, we expect the current bout of inflation to be transitory. It’s likely to remain higher than policymakers would like for longer than they’d like, but the roots are supply constraints which we expect to ease over the coming quarters.

Our real concern in determining strategic asset allocations for our clients is inflation over the next few decades. Looking that far into the future, the range of paths remains wide and uncertain. Our white paper spells out what it would take to put us on courses ranging from the deflationary to the hyperinflationary. Yet we think the most likely courses are more moderate. Notably, the odds of having unusually high inflation have risen to their highest level in many years. That’s no guarantee of high inflation, though—we could quite easily see the Fed succeed in coming close to its 2% target or even undershoot it in the same way that Japan has for decades.

How to Prepare

Should we face a serious or extended inflationary period, either in the next year or at some point over the next several decades, we’d expect traditional asset classes like stocks and bonds to not only perform poorly, but to do so simultaneously, with limited diversification benefits.

To overcome this headwind, inflation-sensitive investors should add other asset classes to their portfolios (Display). These hedges aren’t a panacea. And there are trade-offs. Some add volatility, some underperform in disinflationary environments, some underperform in weak economic environments, and some are simply unreliable. But on balance, we believe that a blend of these assets can overcome these drawbacks and prove worthwhile for inflation-sensitive investors.

Such assets include stocks with pricing power, inflation-protected bonds, inflation swaps, floating rate debt, as well as real assets like commodity futures, real estate, infrastructure, and commodity-linked stocks. Combining them all can increase the robustness and resilience of investors’ portfolios and allow them to successfully navigate the hostile markets inflation may cause.

- Christopher Brigham

- Senior Research Analyst—Investment Strategy Group

- Matthew D. Palazzolo

- Senior National Director, Investment Insights—Investment Strategy Group