As the novel coronavirus quickly evolved into a worldwide pandemic, volatility overtook equity markets. Daily gyrations of 4%, 5%, even 9% became the norm, and pushed the volatility index (VIX) seven times higher. This rapid escalation in risk left many investors wondering how they can combat volatility in their portfolios. The answer may lie with hedge funds. Yet some investors—wary of the asset class due to outdated concerns—have stayed away.

When You Least Expect It

During the decade long bull run, investors let down their guard, especially over the past few years. That’s because risk was nearly non-existent and US equities were on an almost constant upward move, save very short-lived bouts of volatility. Today’s crisis serves as a reminder that volatility can arise swiftly and without warning.

As uncertainty takes hold, there’s a renewed appreciation for diversification and protection in safeguarding assets. Hedge funds not only offer protection from volatile, downward moves, they seem to thrive during challenging periods and provide strong long-term return potential. And while growing pains from 70 years of expansion have left a mark on the industry’s reputation, several critiques no longer seem valid, including the four addressed below:

Myth #1: Hedge funds are more volatile than traditional equities

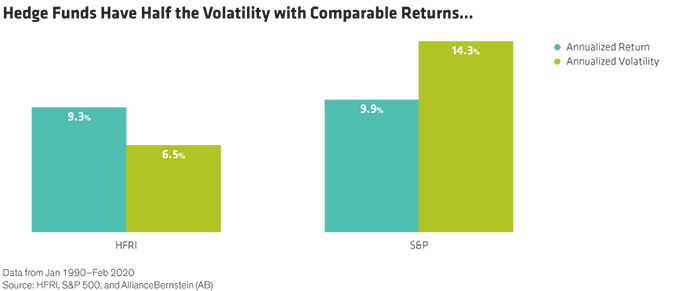

There are many different types of risk in investing. Volatility—or the rapid and unpredictable change in asset values (especially to the downside)—remains one of the most feared. Over the years, hedge funds have developed a reputation for being more volatile than traditional US equities. But is that well-earned? Looking at their returns versus US equities over the last 20 years, we found that hedge funds (as measured by the Hedge Fund Research Index) experienced less than half the volatility of the S&P 500 with only a slightly lower return (Display).

However, this doesn’t tell the whole story. When markets climb, investors tend to worry less about volatility than when markets decline. To assess volatility during difficult stretches (such as economic recessions or market downturns), we considered two periods: 2000–2002 and 2007–2009. During these periods, returns for the S&P 500 fell 24.8% and 38.9 while volatility spiked to 18% and 19%, respectively.‡ By comparison, the HFRI’s returns declined far less, down 0.1% and 12.4% while volatility only rose to 6.8% and 9.1%, respectively.

Downside risk represents another key metric (Display). Volatility stemming from negative moves—or downside deviation—was much higher for US stocks than for hedge funds. That means a 60/40 portfolio of stocks and bonds that adds an allocation to hedge funds can expect a similar return with less than half the risk, especially in down markets.

Myth #2: Hedge funds are just like equities…

One of the reasons hedge funds tend to exhibit lower comparable volatility is because they often invest differently. In other words, the relationship between hedge fund returns and US stock returns is low, depending on the type of strategy. And when markets fall, like they have been during the current COVID-19 crisis, that makes their diversification appeal undeniable.

How does their investment approach differ? There are a number of strategies hedge funds use. A long/short strategy, for example, takes long positions in stocks that are expected to increase in value and short positions in stocks that are expected to decline. Merger arbitrage, on the other hand, bets that companies that have announced a merger or acquisition will complete the transaction with the agreed upon terms. Market neutral funds seek to exploit investment opportunities unique to some specific group of stocks while maintaining a neutral exposure to the market as a whole—by sector, industry, country, and market capitalization.

So, while most equity portfolios struggle when markets experience extreme volatility, many hedge funds shine. In fact, most welcome market swings. That’s because these strategies typically rely on volatility and dispersion between markets or security valuations to drive outperformance. For instance, relative value and global macro strategies benefit when markets experience wholesale sell-offs while acting as arbitrageurs that force asset prices to converge back to fair value.

Myth #3: …but with higher fees

Hedge funds have also been plagued with a reputation for charging high fees via structures that benefit managers at the expense of investors. And historically that may have been true. But over the years, hedge fund fees have come down—and become more transparent. A few decades ago, investors generally paid a 2% management fee and 20% performance fee. But a recent Eurekahedge survey of North American hedge funds noted that the average management fee has fallen to 1.26% while the average performance fee has declined to 14.81%.§ Other investor-friendly mechanisms have also proliferated, like hurdle rates tied to market performance so investors pay based on outperformance, or the alpha that’s produced.

Myth #4: All hedge funds fail

The final misconception is that hedge funds fail at a disproportionately high rate. Is this fair? Not according to research† examining fund defaults based on operational breakdowns and financial losses, including fraud. Operational issues, which account for half to two-thirds of all fund failures, underscore the risk of choosing funds with poor operating controls. This highlights the importance of operational due diligence—doing the homework necessary to pick reputable managers who are operationally sound.

Financial losses are another matter. They’re primarily associated with the risk of losing money due to poor investment decisions or trade executions. This relates to manager skill, and accounts for about a third of failures. These instances reiterate the importance of due diligence—finding managers with disciplined, repeatable investment processes that endure across varied market environments. What about financial losses stemming from fraud? These continue to be uncommon and can also be minimized with ongoing due diligence, including a system of checks and balances between the fund and its independent service providers.

Across the entire hedge fund industry, the risk of financial loss remains quite low. Consider that during the period analyzed, the percentage of funds that failed (for any reason) never exceeded 0.5% in any given year. With roughly 9,000 hedge funds operating today, that would translate to only about 45 funds failures annually. And of those 45, just a small fraction may potentially collapse due to financial losses.

Institutional Controls

Hedge funds have come a long way from their Wild-West past, with undisciplined mandates and fragile (or nonexistent) operational controls. Heightened acceptance by pension funds and other institutional investors has brought greater transparency, improved fee structures, and strengthened operational procedures. Now that some of the industry’s blemishes have faded, once skittish investors can benefit from the inherent advantages of this alternative investing style. The current crisis is a case in point: The US equity market fell over 12% and volatility peaked at 176%* in March, but hedge funds were down only 7% with peak volatility of just 14%.

So as investors wonder how best to combat portfolio volatility, they can answer with more conviction: Hedge funds.

‡Data from 8/31/2000–9/30/2002 and 9/30/2007–2/28/2009

§https://www.eurekahedge.com/Research/News/1920/Hedge-Fund-Fees-Strategy-Profile-July-2019

†Fall 2006 issue of the Journal of Alternative Investments, https://jai.pm-research.com/content/9/2/71 and https://thehedgefundjournal.com/quantification-of-hedge-fund-default-risk/

*Source: Bloomberg. Rolling 5-day realized volatility of the S&P 500 and the HFRX Hedge Fund Index

- Brian Briskin

- Hedge Fund Research Analyst—AB Custom Alternative Solutions

- Michael Heneghan

- Senior Investment Strategist—Bernstein Private Wealth Management

- Wrug Ved

- Senior Investment Strategist—Investment Strategy Group