Over the last decade, investment policies reflected asset allocation rules written at a time when stock returns were strong, and volatility and inflation were unusually low. In that environment, many investment committees abandoned or avoided certain alternative investments that charged high fees and failed to consistently provide superior returns to major stock indices. Looking ahead, however, we foresee the persistence of geopolitical uncertainty as well as rising inflation that can cause markets to become more volatile. And that means the asset allocations that worked well during the last decade probably won’t produce the same results in the next one.

Spending Hampered by the Status Quo

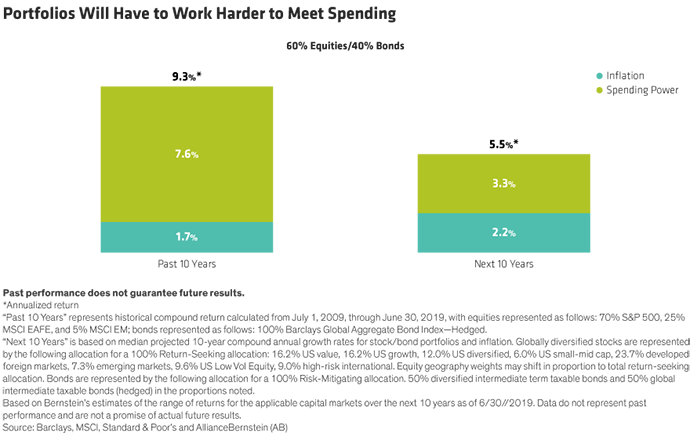

Over the last decade, a nonprofit could spend 7.6% of its portfolio annually and still maintain its purchasing power or inflation-adjusted value. Over the next 10 years, however, we forecast a median projected annualized return of just 5.5% for a typical 60/40 portfolio. Inflation is expected to tick up—to 2.2% from 1.7% —and spending power will be less than half—a mere 3.3% (Display).

In this shifting landscape, it is critical for fiduciaries to explore ways to bridge the gap, so they can meet their investment guidelines and spending needs and achieve their respective missions. Revisiting alternative investments—which we will define as investments with different sources of risk and return than traditional public stocks and bonds—is one such way.

Alternatives Offer a Compelling Argument

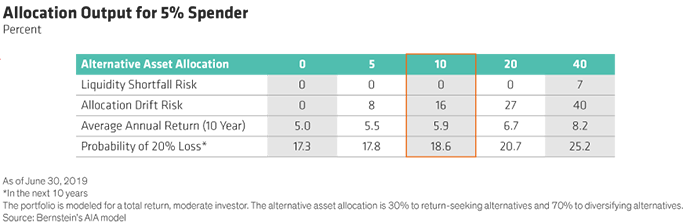

The integration of alternatives offers a compelling argument for organizations seeking stronger returns and less volatility, particularly in a bearish market environment. Below we model scenarios for an investor with a 5% annual spending requirement to show the impact of alternatives on portfolio return and risk (Display). The risk profile for a 5% spender is higher than for an entity that spends less, but the model illustrates that even a conservative allocation is beneficial.

The right portfolio for many foundations and nonprofits spending between 3% and 5% is an allocation of 10% to 20% to alternatives. For the 5% spender example, a 10% allocation makes sense—the portfolio has no risk of running out of liquid assets (no liquidity shortfall risk), an acceptable level of drift (which is the degree to which asset weights drift over time), and a marginal increase in the probability of a 20% drop over 10 years—an increase of 1.3% as compared to a portfolio with no alternatives. Further, a 5% spend can expect an average annual return of 90 basis points higher per year than the no-allocation scenario. For the average 3% spender, the advantages can be even greater.

Four Keys to Success

Nonprofits have unique considerations when determining whether alternative investments fit their investment needs. Below we explore four factors that an organization should bear in mind when considering alternatives.

- FEE STRUCTURE

Alternatives often come with a different fee structure than traditional assets. Understanding how fees are assessed and the expected net-of-fee return is crucial.

Nonprofits can look to lower fees in several ways. In some cases, direct access to an investment strategy, rather than through a third party, may help limit costs. Another cost-sensitive approach may be to accept “beta” or low-cost market exposure where markets are more efficient, such as with large cap developed market stocks. This can shift a greater portion of the “fee budget” towards alternatives with compelling return and diversification characteristics.

- LIQUIDITY

Alternatives are often illiquid investments; many lock up capital for multiple years while others cannot be readily sold on the market. A full understanding of the organization’s liquidity needs and operating reserves is a prerequisite to investing in illiquid assets. As with fee structures, alternatives come with a variety of schedules for funding into the strategy, lock-up periods, redemption windows, and timeframes. It is critical to map capital committed, called, and ultimately distributed out of various investments to available liquid funds.

- REPORTING AND VALUATION

Many alternatives do not mark to market regularly, so there is a natural lag in performance reporting. Thus, communication regarding the timing and methodology of reporting is vital.

Communication between the finance staff and the audit team is important to confirm the valuation of less transparent investments. Lack of foresight and preparation can substantially delay the completion of audited financial statements for key funders and other stakeholders. Janette Burke of Cordia Partners in Washington, DC, attests that “the worst thing is not being prepared for an audit and not carving out enough time to do it. Communication is key. The best clients take the audit process seriously and communicate with the auditor throughout the year, reaching out when things happen or change.”

- TAXES AND UBTI

Two concerns regarding alternative investments are the potential for incurring unrelated business taxable income (UBTI) and the delays in filing the IRS Form 990 due to the timing of the Schedule K-1s. Not all alternative investments generate UBTI, and in some cases, an investment may be sufficiently attractive to justify paying tax on the limited UBTI received. UBTI can be avoided by investing through a partnership that doesn’t use leverage (though that may alter the profile and attractiveness of the opportunity itself); through a structure that can block UBTI, such as a Business Development Corporation (BDC) or a mutual fund; or through an offshore entity that blocks the passage of UBTI to investors.

A Winning Strategy

The integration of alternatives can provide substantial benefits to nonprofits, particularly if the environment gets tougher. But alternatives are not without risks. Consulting with investment, tax, and audit advisors and using analytical tools that can properly project the unique risk and return characteristics are crucial for success. Alternatives can be a winning strategy for many organizations, but education, communication, and transparency are key.

1 2018 NACUBO-TIAA Study of Endowments; 2017 NACUBO-Commonfund Study of Endowments

For more on timely topics for nonprofits, explore “Inspired Investing,” a Bernstein podcast series that covers investing, spending, policy, and more for Endowments & Foundations, and for additional thought leadership, check out the related blogs here. And for more on alternatives allocation, click here.

- Clare Golla

- National Managing Director—Philanthropic Services