With US equities trading at relatively high valuations, earnings growth will be essential for investors to generate returns in 2020. That’s a tall order in today’s environment. Finding standout companies with sustainable growth potential will be especially important.

There’s been plenty of good news for investors in early 2020. The US Federal Reserve continues to maintain a highly accommodative monetary policy. Trade deals are now in place with China, Mexico and Canada. Congress has reached a budget deal. Even amid the highly charged politics of an election year and an impeachment trial, the macroeconomic backdrop is keeping investors upbeat.

Revisiting Market Valuations

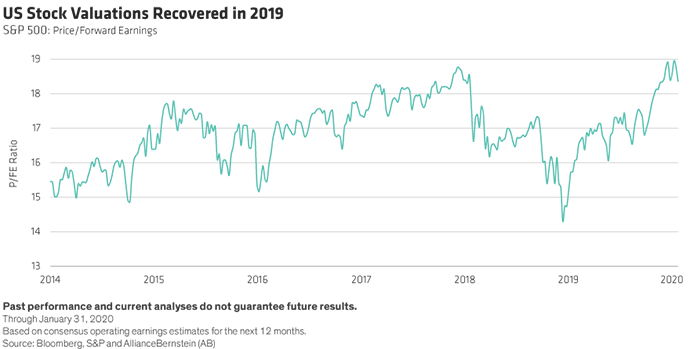

But is the good news already priced into the market? It certainly feels that way with the S&P 500 trading above 18.4 times operating earnings estimates for 2020, through January 31 (Display, below). This is well above the historical average of about 16 times earnings over the past 30 years.

However, equity valuations shouldn’t be viewed in a vacuum. The current interest-rate environment makes a difference for stock valuations. Today, the 10-year US Treasury yield is under 2%, which is well below the long-term average of 4%. When rates are lower, equity valuations should be higher, as investors discount future cash flows at a lower rate, which supports higher stock prices.

Seen in this light, we don’t think current valuations are a risk. Of course, if 2020 earnings falter or inflation picks up meaningfully, we would need to reassess. However, assuming current conditions prevail, additional price/earnings multiple expansion is doubtful, and equities are only likely to rise further from today’s valuations if earnings advance.

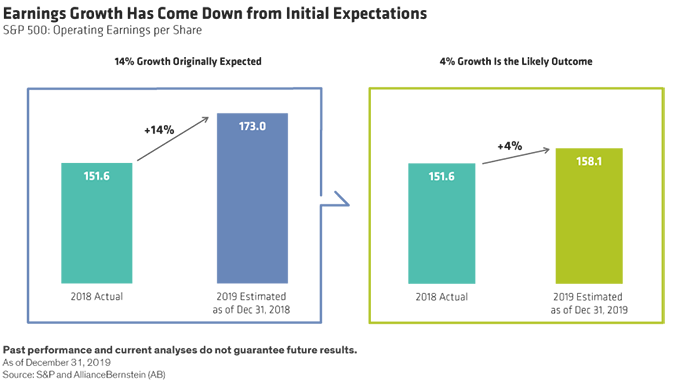

How probable is that outcome? Signals from the broad market aren’t encouraging. Consensus expectations have come down a long way since about a year ago, when US earnings were projected to grow by 14% for 2019. As we progress through fourth-quarter earnings season, it looks like full-year earnings growth will total about 4% (Display, below).

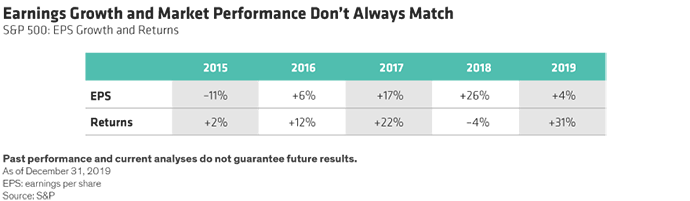

Aggregate earnings growth isn’t a great guide to stock market performance on purely a calendar year basis. Good earnings years sometimes coincide with weak returns, and vice versa. In 2018, the S&P 500 delivered strong earnings growth of 26% but returns were negative. And in 2019, earnings growth was subdued yet stocks surged by 31% (Display, below).

What’s different in 2020? Higher starting valuations raise the risks. Companies are always walking a balance beam, but when valuations are lower, the beam is lower and an earnings miss means a relatively easy fall. When companies falter from higher valuations, the fall can be much more painful for both companies and investors.

Business Fundamentals Will Make the Difference

The best way to avoid these shocks is to focus on fundamentals. Companies in businesses with secular growth drivers that have clear competitive advantages, low leverage and strong management teams are better equipped to deliver sustainable profit gains over time—even in a tougher macroeconomic and market environment.

These characteristics should always underpin a stock selection process, in our view. But after a year of broad market gains, it’s easy for investors to be lulled into a false sense of complacency. Targeting companies that can deliver earnings growth even when it’s hard to come by is a good formula for investing success in today’s challenging growth and valuation conditions.

- James T. Tierney, Jr.

- Chief Investment Officer—Concentrated US Growth