Over the past 30 years—spanning four bull and bear markets—an allocation to cash as part of a diversified portfolio of stocks and bonds has produced lower returns, along with commensurately lower volatility. Yet for nonprofits and foundations, cash has also served as a vital buffer, offering liquidity during times of market stress and a chance to avoid forced selling when spending from their portfolios. That cushion has grown increasingly valuable, especially as choppy markets resurface.

Consider a nonprofit spending 5% per year from a $5 million portfolio, invested in a 70%/30% mix of stocks and bonds. After three decades, adding just a 3%–5% allocation to cash shaved over $1 million from the portfolio’s ending value. Yet this so-called “drag” on performance only yielded modest reductions in volatility. That’s because of the need to replenish the cash allocation, often after depleting it during periods of market stress ( Display).

That dynamic takes on new meaning right now. Spending during a downturn is always tricky, but even more so as nonprofits—and those who fund them—consider increasing distributions to meet today’s overwhelming needs. More than ever, mission-driven organizations need a strategic approach to cash in order to preserve liquidity while minimizing a potential long-term performance drag.

Key Questions for a Savvy Cash Strategy

For board members and investment committees, deploying cash strategically hinges on several key questions. First, what is your current baseline? That requires identifying your current cash positions and where they reside while factoring in your organization’s structure. For instance, certain traditional endowments governed by the Uniform Prudent Management of Institutional Funds Act (UPMIFA) may have lower, more stringent spending thresholds compared to “board designated” endowments or other long-term funds. While the latter have been earmarked for multiyear horizons, they’re not legally restricted in the same way.

Next, establish separate investment pools with distinct purposes, and attach an investment goal (such as preservation or growth) to each (Display). Be sure to include other sources of cash—such as lines of credit, PPP loans, bonds issued, or borrowing (not trading) on margin. For each, note the available balances, any operational issues that could impede access, along with the cost of maintaining such funds.

Avoid Locking in Losses

With your baseline established, it’s time to plan for contingencies. How much cash will you need looking ahead? Most mission-driven organizations set aside sufficient cash to fund fixed operating expenses for a given period (three to six months, for example). But it’s equally important to track the timing of funding those short-term reserves. Do you earmark a given amount monthly, quarterly, or annually? And how do you prioritize revenue sources that may be at risk and require backfilling with cash?

Consider a nonprofit advocating for women in the arts. To ensure the vitality of their mission, the board prudently set aside three months of fixed operating expenses—funded monthly. But they overlooked a contingency plan to protect fundraising revenues. After canceling their annual spring gala due to the pandemic, the nonprofit was forced to tap their investment portfolio to maintain its programming. Unfortunately, with the market sinking at the time, they locked in losses, creating an even bigger hole to fill.

Know the Trade-Offs

How can the board avoid a repeat scenario? By adopting a strategic approach to cash covering all spending needs. That means working with your financial advisor to proactively plan for sourcing cash from different asset pools. Below we outline several prompts to help you get started:

- How much do you want to set aside (one year’s spending, one quarter?)

- How often will you replenish? For instance, will you top it up when it falls below a certain threshold (i.e., 50% of the original allocation) or wait until it’s fully depleted?

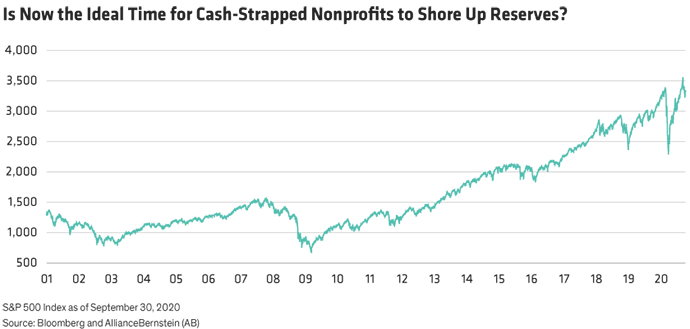

- If you’re currently facing a cash crunch, when should you begin shoring up reserves? Now may be the ideal time given that markets are hovering near all-time highs—and bracing for near-term volatility due to political and economic headwinds (Display).

Clearly, liquidity plays a central role in ensuring your organization’s overall financial health and vitality. Prudent management involves building and implementing a strategic plan for cash—one that strikes a balance between protection and maximizing long-term growth. With savvy positioning, cash can be a lifeline without being a drag.

- Todd Buechs

- National Director, Core Fixed Income & Alternative Credit—Investment Strategies Group

- Clare Golla

- National Managing Director—Philanthropic Services