The $2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act—the third emergency bill in response to COVID-19—goes beyond private sector bailouts. The CARES Act recognizes the vital role nonprofits play, too. To ensure they can continue to provide critical assistance to their communities, the bill relaxes some of the limitations on charitable income tax deductions for individuals and corporations, and provides nonprofits with access to capital--welcome relief for organizations starved for funds.

Tax Breaks for Givers

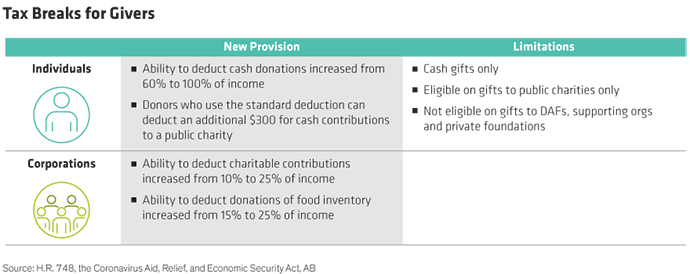

With donors needed now more than ever, the CARES Act aims to encourage charitable giving by revisiting tax incentives (Display). For individual donors, deductions on cash gifts had previously been limited to 60% of adjusted gross income (AGI). Now this limitation is suspended for this year, effectively raising deductions to 100% of income.

But only cash contributions to public charities are eligible for the higher limit; gifts to donor-advised funds, supporting organizations, and private foundations do not qualify. Taxpayers who don’t itemize their deductions also receive a benefit. Donors who use the standard deduction are permitted to deduct an additional $300 for cash contributions to public charities this year.

The exceptions aren’t just aimed at individual donors. For corporations, the deduction for charitable gifts is now increased from 10% to 25% of taxable income. The bill also increases deductions on food contributions from 15% to 25%.

Relief for Organizations

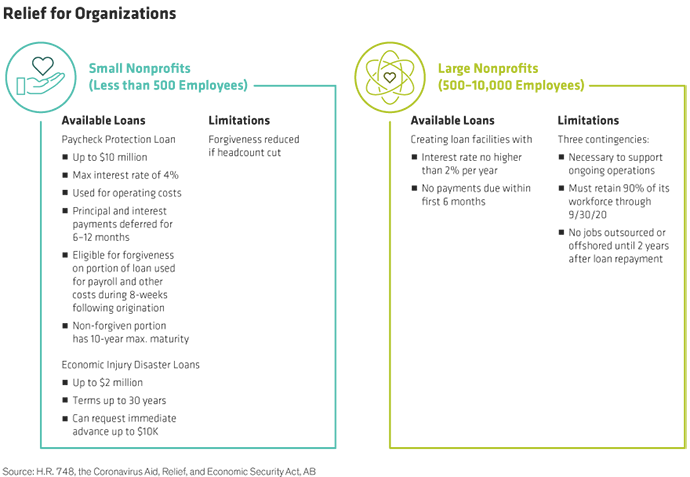

What about nonprofits themselves—and the millions of workers employed by them? These mission-driven organizations also benefit from the recent legislation, but the provisions differ depending on the organization’s size (Display).

For small nonprofits—organizations with less than 500 employees—CARES creates a new Paycheck Protection loan program through the Small Business Administration (SBA). These low-interest loans of up to $10 million* can be used to pay operating costs, such as payroll, mortgage, rent, utilities, and insurance premiums. No collateral or personal guarantee is required, and principal and interest payments can be deferred for 6–12 months.

Small nonprofits may also be eligible for forgiveness on a portion of the loan used for payroll and other costs during the eight weeks following the loan origination. However, forgiveness may be reduced if headcount is cut. In other words, a nonprofit can effectively turn a portion of the loan into a grant by keeping its staff on payroll. Any loan amount not forgiven would have a 10-year maximum maturity.

Additionally, under Congress’s second emergency bill, the SBA expanded the program for Economic Injury Disaster Loans (EIDLs). Those eligible small nonprofits can apply for loans up to $2 million, based on the economic injury incurred. Repayment periods are as long as 30 years with terms determined on a case-by-case basis, based on each borrower’s ability to repay. The interest rate is 2.75% for nonprofits. This program allows an eligible entity to request an immediate advance on the EIDL of up to $10,000. An applicant would not be required to repay an advance payment, even if it is subsequently denied an EIDL. Borrowers can apply online at https://www.sba.gov/page/coronavirus-covid-19-small-business-guidance-loan-resources.

For larger nonprofits—organizations between 500 and 10,000 employees—CARES provides access to a specific loan facility at a rate no higher than 2% per year, with no payments due for the first six months. Borrowers must certify three contingencies: (i) the loan is necessary to support ongoing operations, (ii) the organization will retain 90% of its workforce until September 30, 2020, and (iii) no jobs will be outsourced or offshored for a period ending two years after repayment of the loan.

CARES Helps You Care

The government has acted swiftly in the wake of this crisis, providing stimulus to American businesses and individuals. Hopefully, the aid will encourage charitably inclined Americans to donate to causes in this time of need and provide nonprofits with access to the funds necessary to retain staff and continue their important mission-related work. Because, as we’ve seen so many times in the past, it’s acts of goodwill that accelerate change.

*Paycheck Protection Loans have maximum interest rates of 4% and amounts are tied to payroll costs.

- Christopher Clarkson, CFA

- National Director, Planning | Foundation & Institutional Advisory