The end of the year may be your last chance to take advantage of strategies to lower your tax bill for 2019. But don’t wait till the last minute. Find out if these strategies are appropriate for you.

Have you maximized tax-deferred savings vehicles?

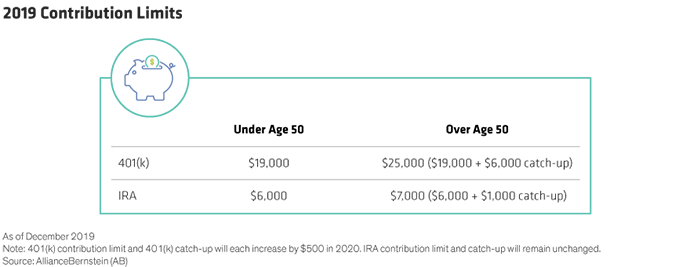

In many cases, getting the most out of tax-deferred savings can make or break your long-term investment success. Contributing the highest amount will not only increase your savings, but also lower your taxable income.

Married couples filing jointly also have another option that is often overlooked. A working spouse can make a full contribution to an IRA on behalf of a non-working spouse under the age of 70½. The entire contribution remains deductible, provided neither the IRA owner nor the spouse actively participates in an employer-sponsored retirement plan. Otherwise, the tax deductibility of the contribution phases out at higher income levels. Business owners seeking a larger tax deduction can also take advantage of the higher contribution limits for other retirement vehicles. For example, the IRS allows business owners to contribute the lesser of 25% of compensation, or $56,000 annually to SEP IRAs and defined contribution plans. Contribution limits on defined benefit plans, including Cash Balance pensions, can be even higher.

Did you take your Required Minimum Distributions?

Investors should generally preserve funds inside retirement plans for as long as possible. However, some have no choice: IRA owners over age 70½ and beneficiaries of inherited IRAs must take Required Minimum Distributions (RMDs) by December 31 each year. The lone exception is the first required distribution, which must be taken by April 1 of the following year. Those missing the annual deadline face severe penalties: a 50% excise tax on any shortfall in the distribution.

What’s the most tax-efficient way to make a charitable donation?

Donors can help themselves—while helping others—by making charitable contributions in the most tax-efficient way possible. In most cases, that means donating appreciated securities, rather than giving cash. That way, donors receive a charitable deduction for the value of the securities while avoiding tax on the appreciation. The catch? Avoid contributing appreciated stock held less than one year, because the deduction for a short-term security is equal to its cost basis, not its current value.

What about for donors who are taking the standard deduction?

Bunching multiple gifts into a single year can increase the tax benefit of charitable gifts in certain years. And if they don’t want the charity to receive the gifts all at once—or if donors have unusually high income or gains this year—they could fund a donor-advised fund (DAF).

Another attractive option for donors taking the standard deduction? Individuals over age 70½ can donate up to $100,000 from their IRA. The gift must go directly to a charity, rather than to a DAF or private foundation, and will qualify as part of the donor’s RMD. Plus, the distribution is excluded from gross income—providing the equivalent of a 100% deduction.

Do you need to offset realized investment gains?

Equity markets have surged since 2009 and many investors hold positions with large gains. Mutual funds are required to distribute realized capital gains and income as dividends, which creates a taxable event for fund shareholders. Some of these can be offset by harvesting losses. A net loss of up to $3,000 can also be used to offset ordinary income.

Have you considered gifting to family?

The current annual gift tax exclusion rests at $15,000 per person ($30,000 per couple). In addition, the gift and estate tax exclusion—as well as the generation gifting transfer (GST) exemption—currently stand at $11.4 million per person.

Many of the hurdle rates for wealth transfer vehicles remain low by historical standards. Since its establishment in the late 1980s, the 7520 rate has averaged approximately 5.2%. Yet today, the rate is only 2.0%.* What’s more, the rates used to calculate intrafamily loans and sales remain highly attractive.

In the current environment, leveraged strategies like loans, installment sales, or grantor retained annuity trusts (GRAT) seem preferable to outright gifts. Plus, a loan or installment sale gives the grantor the option to forgive the debt and complete the gift if it appears that Congress may reduce the exclusion amount in the future.

Tailored for your needs

Tax efficiency is an important component for any wealth planning strategy. It’s about taking advantage of contribution limits, and choosing the right vehicles, assets, and strategy. These are just five things to think about before year-end, but a financial advisor can help you devise a plan that’s just right for you.

*November 2019 rate

- Christopher Clarkson, CFA

- National Director, Planning | Foundation & Institutional Advisory

- Tara Thompson Popernik

- Head of Wealth Strategies