Thrill-seekers often experience an anticipatory rush before stepping in the ring. But others feel a different type of “gut reaction”—one closer to queasiness. What does that have to do with investing? Investors frequently have similar reactions when the market makes big moves. While the prospect of victory seems thrilling, being on the ropes can be downright nauseating.

Some investors take the gyrations in stride, knowing that markets trend higher over time. But most—especially those who count on their investments to support spending needs—feel a creeping sense of panic. How can you avoid being floored by extreme fluctuations in public markets? Consider illiquid alternatives.

What’s the Alternative?

“Alternatives” is a catch-all term for asset classes that defy categorization into public equity or public fixed income. Alternatives include tangible, real assets like commodities and real estate, private market investments like private equity or debt, as well as leveraged public market assets—that can buy long and sell short—such as hedge funds. Each alternative asset class has discrete performance drivers that differ from traditional bonds and equities, and importantly, from other alternatives. Those unique drivers create a diverse relationship or correlation with other assets.

Five Contenders

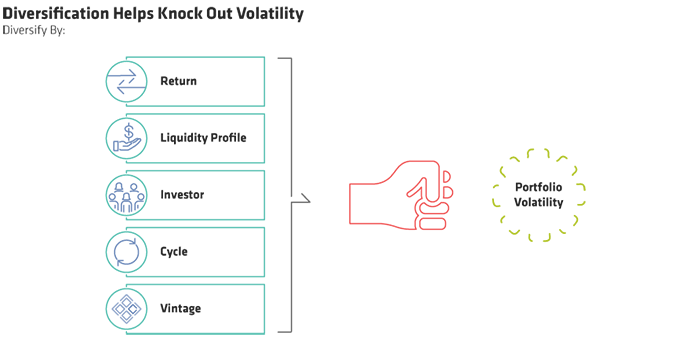

Illiquid alternatives offer five distinct opportunities to diversify risk (Display), providing an effective counterpunch to volatility. Let’s explore each in turn:

Return: Here’s one top-of-mind question many investors ask: How can I harness unrelated return streams so that my portfolio can weather down markets? In the past, investors tried to diversify returns by adding investments from disparate geographies, company sizes (capitalizations), or styles (growth or value). But those asset classes haven’t consistently delivered the diversification investors craved. That’s because, over the long-term and especially during violent downturns, they tend to move in tandem.

But adding alternatives—like private real estate—where the underlying source of return has a low correlation to public markets can enhance diversification.

Liquidity profile: Public securities trade throughout the day, whereas alternatives offer limited liquidity. For example, investment dollars in private market alternatives help build businesses over time. For that reason, these strategies are best suited to investors with long horizons who can wait to realize those returns. In exchange, investors demand extra compensation for having their investment dollars tied up for lengthy periods. This extra payoff—an illiquidity premium—rewards investors for the loss of access to that capital, while diversifying the portfolio overall.

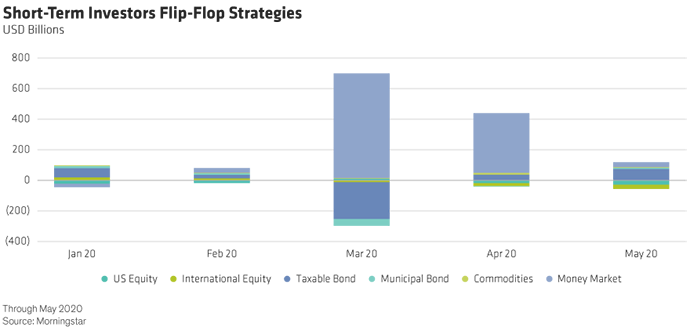

Investor: Alternative funds generally have specific mandates, which tend to attract like-minded investors. In contrast, it’s difficult to gauge whether fellow investors in publicly listed stocks and bonds are long-term holders or short-term traders. Owners of public securities may have different time frames and goals for their holdings, which often leads to untimely entrances and exits, potentially harming performance. The impact of this mismatch is most pronounced in volatile markets. For instance, as the markets grappled with the effects of COVID-19, investors indiscriminately sold taxable and municipal bonds before the pandemic’s effects could be fully ascertained. And the downward moves intensified as other investors panicked and began selling too (Display). Once calm was restored, investors reversed course. But those who sold into the drop likely missed out on the subsequent rally as they tried to time their re-entry.

Steep sell-offs sparked by market declines do not occur with illiquid alternatives. Of course, like any investment, they can lose money—but not due to panic selling in market pullbacks. And although some illiquid strategies mark the value of their holdings up or down based on similar public securities or commodity prices, those marks remain unrealized. In other words, they only exist on paper. Unrealized changes in the value of private investments don’t reflect the actual exit price an investor could secure on a disposed asset. In contrast, moves in the public markets are always real changes to an investment’s value. Long-term investors tend to favor that private market approach, and the strategies benefit from their investors’ homogenous nature .

Vintage: Many types of alternatives—like private equity, private lending, venture capital, and real estate funds—have multi-year horizons. The year the fund makes its first investment marks the vintage year, and each vintage enjoys distinct market conditions that vary. Put another way, spreading investment dollars over several vintages provides a built-in level of diversification. In public markets, an investor can only attain vintage diversification by dollar-cost averaging or buying market dips. To succeed, an investor must continually add new capital, which can be emotionally challenging when markets fall.

Cycle: Funding for new private equity, real estate, and private credit strategies tends to be negatively correlated with unfavorable environments—when markets become rocky or expensive, strategies are often shelved to await more auspicious conditions. As a result, these funds typically avoid the top and bottom of the cycle, so an allocation is likelier to occur at a more optimal entry point. Carefully weighing when to dip into the market also fosters a ‘dry powder effect’ as these strategies typically buy when other investors are fearful and pulling back. So, whereas public market investors fear bad markets, private market investors look forward to the attractive entry points they bring.

Fighting Bouts of Volatility

With illiquid alternatives, the best results come from putting money to work at different stages in the economic cycle. While not unique to nonpublic asset classes—many investors subscribe to dollar-cost averaging—alternatives innately do the work for you. Our natural fight or flight tendencies usually cause us to flee when the going gets tough and add more when good times resume. Yet vintage and cycle diversification, in addition to the liquidity profile of alternatives, keep those harmful tendencies in check. So instead of boxing yourself in a corner, consider dealing a decisive blow to volatility with illiquid alternatives.

- Alexander Chaloff

- Chief Investment Officer & Head of Investment & Wealth Strategies