We’re surrounded by constant reminders these days that unexpected events can happen at any time. And while there are some things you cannot plan for, your estate represents one where you can. Most individuals don’t like to contemplate their ultimate departure but avoiding the topic altogether can complicate life for those left behind. Here’s a quick overview to set the process in motion.

Estate Planning Basics

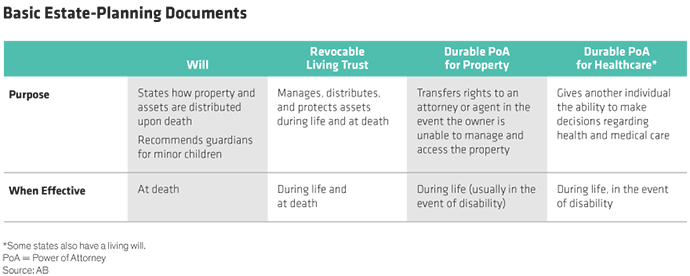

Proper estate planning ensures that when you die or become incapacitated, you retain control over who receives your property, how beneficiaries might obtain and use inherited assets, or who cares for you, your minor children, and your property. To accomplish this, there are four basic documents you should have—a will and/or revocable living trust, durable power of attorney for property, and durable power of attorney for healthcare* (Display).

What Can Go Wrong?

Plenty.

Without a legal blueprint, your assets can go to unintended beneficiaries, or the state may decide what happens with your estate. And if the courts intervene, it will likely exact a heavy financial and emotional toll on your loved ones. In some cases, it may take months or years to distribute the assets. So whether you lack one or more of these documents (or even if you have them), review and update them regularly as life conditions—such as having a baby or selling a business—change. Below we share two examples of what can happen without a proper plan:

No will or trust: Your will determines where your assets go, and who will care for your minor children. What if you have an asset not included in your plan? If that asset doesn’t transfer by title, doesn’t have a named beneficiary, or is not owned by a trust, it will go to probate where it could pass according to state law, rather than your wishes.

Musician Prince is a prime example:

- What happened: His $200 million estate was subject to Minnesota laws of intestate succession. It is believed that Prince had no spouse or children, and under intestate succession, charity is not a beneficiary. His lack of planning means that half of his assets went to pay state and federal estate taxes, while bankers, lawyers, and consultants earned millions. His six siblings/half-siblings received the remaining assets.

- Lesson: Dying without an estate plan means an external party determines who inherits your assets. This can take years and lots of money to sort out.

Failure to select beneficiaries: Choosing the right beneficiaries is crucial. As is updating your estate plan when you have a life change, like a marriage, divorce, or with the birth of a child. When unwanted beneficiaries are still named, assets will be transferred to them, even if the deceased intended to leave them to others. So keeping your estate plan current remains critical.

Actor Heath Ledger and singer Barry White offer two cautionary tales of what happens when you neglect your estate after a life change:

- What happened: Heath Ledger drafted his will before the birth of his daughter, leaving all assets to his parents and three sisters. After his untimely death, his two-year-old daughter and her mother received nothing. Though ultimately, his family chose to give the entire estate to his daughter. Barry White’s second wife inherited his entire estate, despite being separated from the singer, while his live-in girlfriend of several years and nine children received nothing. This created a legal battle between his second wife, girlfriend, and children.

- Lesson: Review and update estate-planning documents and named beneficiaries after major life changes (marriage, divorce, birth of children, etc.). During a divorce proceeding, however, options for limiting a soon-to-be ex-spouse’s inheritance are constrained. Think about signing a prenuptial and postnuptial agreement before entering into marriage.

What to Consider

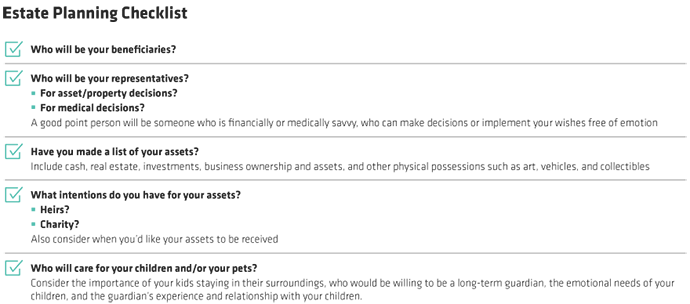

Before you prepare your estate documents, introspectively examine how you want your assets used, who might make an optimal guardian, and how you want to live should you become incapacitated. To go down the right path, consider these prompts (Display):

Coming to Grips with Mortality

It’s hard to envision not being part of loved ones’ lives. But being left behind is even more difficult. Don’t make it tougher by failing to establish or revise your estate plan. Whether you aspire to leave money to heirs, charity, or both, your wishes will only be honored with proper and legal estate plans. Such plans will also ensure you don’t lose control over how your hard-earned assets are allocated and used. Now is the time to act, because as this crisis makes clear, life is already uncertain; don’t let your estate plan be, too.

*Some states have a separate living will and others include it as part of the healthcare power of attorney.

- Emily Neubert

- Senior National Director—UHNW Services