The coronavirus outbreak and resulting collapse in financial markets walloped investors around the world. The blow hit nonprofits twice as hard, given their need to plug newfound financial gaps. In response, many nonprofit board members have already taken immediate steps, like revisiting Investment Policy Statements and reviewing spending. But investment committees should also consider timely opportunities that have arisen from the reordered investment landscape.

For instance, risk assets now offer better rewards than they have in the recent past, provided you have sufficient near-term liquidity and a long-term investment horizon. But which risk assets? In past posts, we’ve made the case for private assets. Today, we recommend a fresh look at high-yield debt. While high-yield bonds suffered in March as spreads widened, their prices haven’t rebounded nearly as much as US equities.

Is High Yield Right for Your Organization?

Stubbornly low interest rates still have many investors reaching far and wide for yield. As a result, some investors are reconsidering their fixed income exposures—whether US Treasuries or investment grade credit—while still acknowledging the critical role that fixed income plays in their portfolios.

For others, high-yield corporate bonds seem like a bridge too far. Are they too risky? Do they hold up in volatile markets? Are they inferior versions of equities, as some prominent endowment CIOs have argued in the past?

In fact, high-yield bonds have historically performed predictably—even in challenging market environments. That’s because high-yield bonds provide a consistent income stream that few other assets can match. And since tax-exempt organizations don’t have to worry about paying taxes on the high amount of interest income, they fit remarkably well in nonprofits’ portfolios.

Plus, when high-yield issuers call their bonds before maturity, they pay bondholders a premium for the privilege. This helps compensate investors for losses suffered when some bonds default.

What does all this mean for today’s investors? High-yield bonds may experience additional volatility, but for those with a long-term lens, they could offer key advantages that today’s investors crave.

Finding the Best Fit

Consider high-yield debt if you:

- Want to put new money to work in risk assets but are worried about equity volatility

- Want to diversify equities without giving up expected return

- Want more income

1. High-yield bonds can be a great substitute for US stocks. Most investors consider high-yield bonds part of their fixed-income allocation. But they act more like equities. That’s because, like stocks, high-yield bonds are strongly linked to the business results and fundamentals of the companies they represent. Those reconsidering fixed income amid persistently low rates may want to keep this aspect in mind.

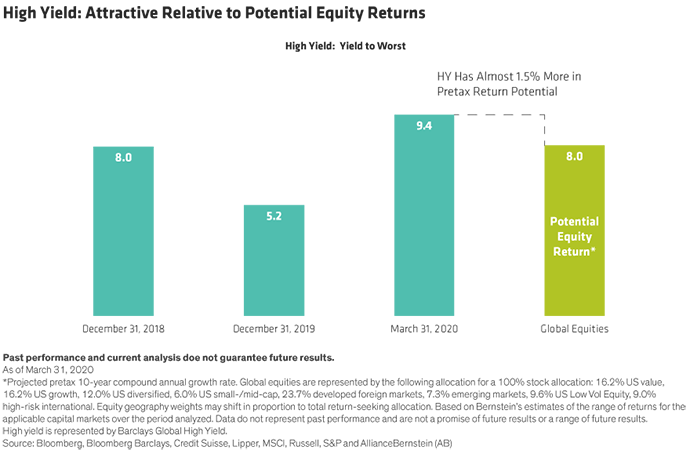

There’s one important difference, though. Over the long run, high yield has produced equity-like returns with half the volatility of stocks (Display). When high-yield spreads are wide and equity valuations are stretched, like today, introducing high yield into your mix may prove ideal.

History has shown that US high-yield bonds lose less than US stocks during downturns and recover those losses more quickly. A big reason for that? High yield’s steady stream of interest income that gets paid in bull and bear markets alike. And as long as an issuer avoids bankruptcy, investors get their money back when the bond matures.

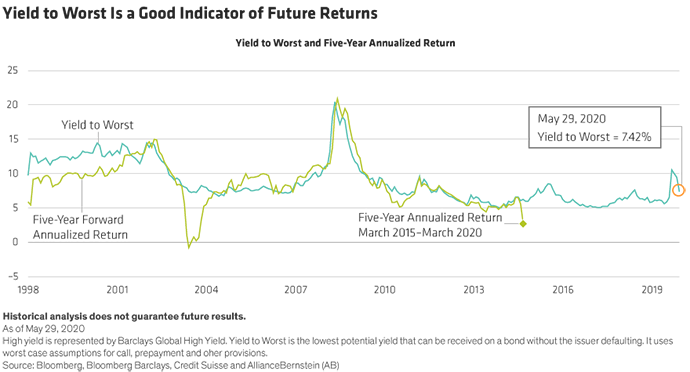

2. Ample yields already compensate investors for higher defaults ahead. Global high-yield spreads recently hit more than 10%—well above their long-term median of 4.9%. As the markets have regained confidence, both stocks and bonds have rallied from their lows. At current levels, high-yield corporates appear attractively priced, but it’s important to recognize their much higher default potential compared to just three months ago. We’re expecting a spike in defaults to around 8%–12%, depending on the length and depth of the downturn. But ample yields already compensate investors for significantly higher defaults ahead. And remember, a high-yield portfolio’s starting yield has been an excellent proxy for return over the next five years (Display).

3. At current levels, high-yield bonds could outperform stocks over the next few years. Generally, we’ve found that the yield you start with at the outset represents a pretty reliable indicator of what you could expect to earn over the next five years. The yield-to-worst for the broad global high-yield market—the lowest likely return you should get barring defaults—recently hit levels that should exceed forecasted returns for bank loans or passive equity strategies.

4. High yield usually does well when interest rates rise. Rising rates are probably the last thing on bond investors’ minds right now, though someday that worry might return. Yet rising rates usually go hand in hand with faster economic growth, and faster growth tends to boost corporate profits. This helps explain why high-yield bonds are generally not as correlated to interest rates as investment-grade bonds. And if anything, income-oriented investors with long investment horizons should root for higher rates. When their bonds mature, they can reinvest the proceeds into newer and higher-yielding bonds, likely increasing their total return.

It Still Pays to Be Selective

While rising rates aren’t yet a concern and defaults appear well compensated, investors can’t afford to be cavalier. Selectivity remains vital and a global, multi-sector approach makes sense, given the disparate pace of recovery across sectors and geographic regions. Whether looking to make a long-term commitment to the asset class—or just benefiting from returns expected to be higher than stocks for the next period of years—high yield is a resilient asset class that can reward selective nonprofit investors.

- Greg Young, CFA

- Senior Investment Strategist

- Christopher Brigham

- Senior Research Analyst—Investment Strategy Group