Private markets have afforded investors the opportunity to financially and operationally improve businesses for the long-term, without the pressures to meet short-term—typically quarterly—performance metrics. This longer horizon provided private equity investors with returns superior to public equity equivalents. However, in the decade following the Global Financial Crisis, public markets performed exceptionally well, and the S&P 500 outperformed the private equity market. As a result, some are reconsidering the merits of the asset class, throwing aside its numerous beneficial characteristics. In this series of blogs, “PE Mythbusters,” we address today’s objections and commonly held beliefs—many of which are incorrect— about private equity. These blogs are not making a call on when or how much to allocate to private equity, or saying that private equity is universally appropriate. But it will remind investors of the merits of the asset class and provide a compelling case as to why some investors may be missing an opportunity if they don’t have an allocation.

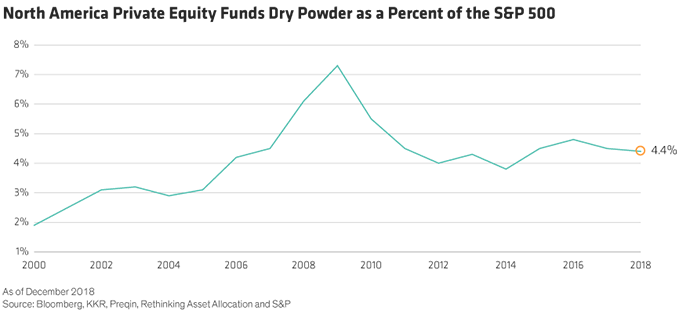

Some observers cite $1.2 trillion of dry powder standing ready to be put to work by private equity (PE) funds. Others report $2.5 trillion. Regardless, the figure is significant and has increased over time (Display), at least equivalent to 4.4% of the S&P 500.* With this much cash needing to be invested by funds eager to generate returns and associated fees, some fear PE is a crowded trade and may cause them to chase bad deals. We disagree.

The Argument

Today investors are concerned that the $1.2 trillion* of uninvested capital—which is more than double the amount from just six years ago—will force funds to become irrational and undisciplined. Data seem to support this view: Purchase price multiples for buyout funds averaged 11.2x through the first nine months of 2019, up 6% from the year prior, and almost double the lows after the Global Financial Crisis (GFC). While this can seem worrisome, when put in perspective, there is less cause for alarm.

Five Counterarguments

There are five reasons why the levels of dry powder and today’s valuation multiples should not negate considering an allocation to private equity.

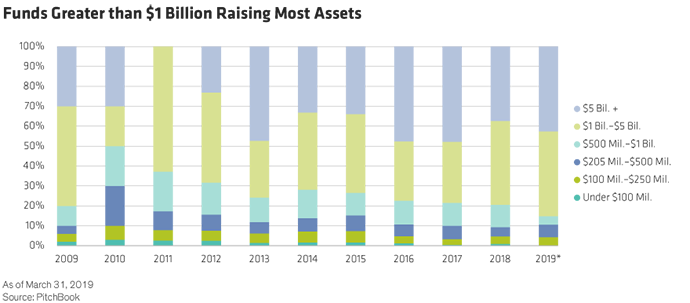

Dry powder concentrated at the top: Not all firms have an irrational overabundance of cash. Funds greater than $1 billion are fundraising at a disproportionate rate as compared to the smaller funds (Display). In fact, four publicly traded private equity sponsors disclosed at the end of 2019 that, collectively, they control $223 billion of dry powder. Conversely, most small to mid-sized funds have a sensible amount of available capital that will allow them to invest rationally and without haste.

Larger companies=Larger deals: Improved operating performance and supportive capital markets have dramatically increased the size of companies since the financial crisis. Ten years ago, a company was considered small-cap† if it had a market cap of $1.2 billion; today, that same cutoff is $3.6 billion. Said a different way, today companies can be considered “small” at triple the size of 10 years ago. So, PE funds need to write bigger equity checks to purchase them. Therefore, the size of the dry powder seems more appropriate.

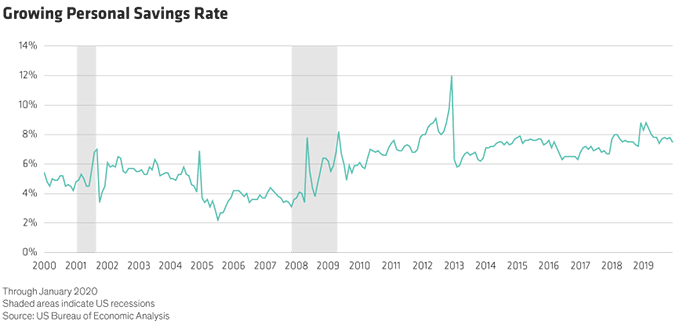

Cash everywhere: The amount of committed capital is staggering, but private equity firms are not alone in holding high levels of cash. Since even before the GFC hit, personal savings in the US have been rising. At the beginning of 2000, the personal savings rate was 5.4% before dipping to the lowest level in 60 years, 2.2% in July 2005. Today that rate is hovering around 7.8% (Display). Does this mean households have too much dry powder?

Similarly, cash on balance sheets of the US’ largest companies has been growing. Cash as a percent of total assets has nearly doubled—from 5.6% in March of 2007 to 10.8% at the end of January. So, while $1.2 trillion may seem like a lot, the fact it doubled over the past six years should not be concerning because it is consistent with savings levels from other sectors of the economy.

PE is putting money to work: While the absolute level of dry powder has grown, PE has been putting money to work at a faster pace, justifying the substantial uncommitted capital. According to a 2018 Bain & Company report, private equity had 3.0 years of capital supply, lower relative to the high of 4.6 years in 2007–2008, implying that the industry is under less pressure to spend today than it was a decade ago.

Not everyone’s in a rush: The amount of dry powder may be the wrong focus; why it’s higher seems to be the more important question. For many, the reason is simple—41% of private equity firms surveyed said that they were raising more capital to have cash on hand for tougher times ahead.‡ Taking advantage of market dislocations is key to making profitable investments. So, a fund that has the capital to pull the trigger when everyone else is running for the hills should be able to invest in strong companies at fire-sale prices and obtain a robust return. So, perhaps the pressure to invest the available funds is not as elevated as many believe.

PE Investing Requires Patience and Precision

We offer two pieces of advice when considering a PE investment. The first: Go small. Mega funds are raising more and more capital, and that may put pressure on them to get deals done. Smaller funds are under far less burden. Our second piece of advice: Be patient. Private equity funds have relatively long lock-up periods for a reason—because they need time to find suitable investments, make those investments work, and dispose of them. When one invests in a private company, the time frame for harvesting that investment is much longer than in public markets, but unlike others calling PE a “crowded trade,” we think it’s worth the wait.

*As of end of December 2018

†Based on Russell index methodology

‡ https://www.bdo.com/news/2019-december/bracing-for-a-bear-market,-private-capital-readies

- Alexander Chaloff

- Chief Investment Officer & Head of Investment & Wealth Strategies