Recent changes to the Internal Revenue Code have breathed new life into the Qualified Small Business Stock (“QSBS”) exclusion—and it clearly merits a second look. Investors, founders, or employees who receive stock in small businesses may be eligible for significant tax savings, if certain requirements are met.

An “Exclusive” Club

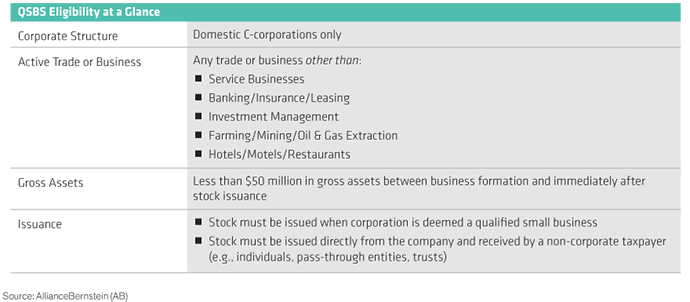

For stock to be considered for the QSBS exclusion (Display), it must be:

1. Issued by a “small business”

2. Granted by a business that is “active” for substantially all the owner’s holding period

3. Received by the owner at “original issuance”

Let’s walk through each in turn.

Small Business Test

To satisfy the small business requirement, the following two criteria must be met:

1. The stock must be issued by a domestic C corporation and cannot be structured as a DISC, RIC, REIT, REMIC, or Cooperative

2. The business must have less than $50 million in gross assets at all times between its formation and immediately after stock issuance. What constitutes gross assets? Cash and the fair market value of any assets the corporation received in exchange for stock at the time of the contribution. If the corporation owns more than 50% of a subsidiary company, all the subsidiary’s assets are included for this litmus test, too.

Importantly, the gross asset requirement is not based on the fair market value of the business at the time of issuance. Stock issued that satisfies the asset test will continue to be treated as QSBS even if the corporation’s gross assets eventually exceed $50 million.

Active Business Test

Size and structure represent important criteria, but it doesn’t end there. That’s because Section 1202 imposes two further requirements. The corporation:

1. must use at least 80% of its assets in the active conduct1 of a qualified trade or business, and

2. cannot be a trade or business that is explicitly disqualified2

What types of businesses fall into the latter category? Generally speaking, service businesses in specified fields or businesses where the principal asset is the skill or reputation of one or more employees. This includes businesses involving finance or investment management, farming, mining, or the operation of a hotel, motel, or restaurant.

Original Issuance Test

Once deemed a qualified small business from earlier tests, a final hurdle remains. To satisfy the original issuance test, the stock must:

1. Be issued by a domestic C corporation1

2. Be issued directly from the company or from an underwriter (secondary acquisitions do not qualify) to a non-corporate taxpayer, such as individuals, pass-through entities, and trusts

3. Be received in exchange for money, other property (not including stock), or as compensation for services provided to the corporation

Making the Grade

How might this play out in practice? Consider the following pass/fail scenarios.

Pass: Steve founded a small business that manufactures and distributes organic pet food. Steve formed his company as a C corporation and received his shares directly from the corporation in his revocable living trust. Steve’s shares meet the test for original issuance.

Pass: Andi invested $5 million in a fast-growing robotics company in exchange for preferred stock, bringing the gross assets of the business to $20 million. Two years later, the company’s gross assets have tripled to $60 million. Andi’s stock remains eligible for the QSBS exclusion because the company had less than $50 million of gross assets immediately after the issuance of her preferred stock.

Fail: Pavan founded an executive recruiting business that specializes in placing candidates in the healthcare sector and formed his business as an S corporation. While his firm meets the “small business” test, it fails the “original issuance” test because shares were not issued from a domestic C corporation, nor would it qualify as an “active business” because it is a service business that principally relies on his expertise.

The Devil Is in the Details

As these examples show, applying these tests to a specific company or stockholder’s stock is often more complex than it appears. Given the powerful tax incentives on the table, consider engaging qualified tax and legal professionals sooner rather than later. In our next post, we’ll revisit the original issuance test and unpack some of the more important details associated with business entity choice.

Business owners deserve a partner who will support them right from the start. For more thought leadership for entrepreneurs and business owners, check out the related blogs here.

- Stephen Schilling

- Director—Wealth Management Group

- Andrea Ross

- Director—Wealth Strategies

- Pavan W. Auman, CFA

- Director, Tax & Transition Strategies—Wealth Strategies Group

1 Notably, the corporation must meet the active business test and be a domestic C corporation for “substantially all” of the stock owner’s holding period (although “substantially all” is not defined in the Internal Revenue Code or regulations). See IRC 1202(e).

2 See IRC 1202(e)(3) for a complete list of disqualified trades or businesses.