Americans quickly mobilized this year with a generous outpouring of support for those rocked by the pandemic, natural disasters, and societal unrest. And the CARES Act offered crucial incentives encouraging donors to dig deep. But some provisions are set to expire at the end of this year.For those who haven’t explored the benefits, the time to act is now.

Charitable Planning Under the CARES Act

The CARES Act offers tax incentives for cash contributions made to a public charity.* For instance, whereas deductions on cash gifts had previously been limited to 60% of adjusted gross income (AGI), now donors who itemize can deduct up to 100% of taxable income this year only.** This benefit only applies to cash donations; the CARES Act does not amend the tax deduction for gifts of appreciated securities to public charities (where the deduction still stands at 30% of AGI).

Make the Most of the New Deduction Limit

While the new AGI limit is inherently compelling, dividing charitable gifts across various assets and giving vehicles can further boost the benefit. Here are timely strategies to help maximize the soon-expiring CARES Act provision.

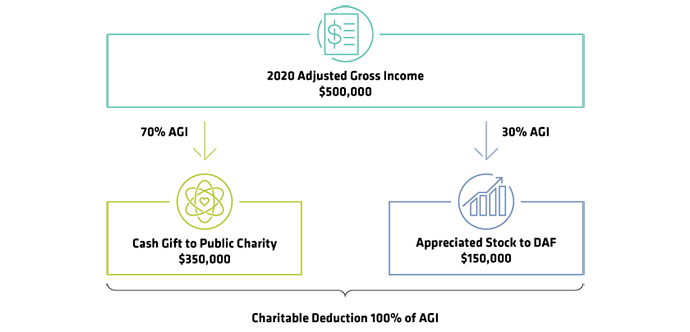

- Give more, and use the charitable deduction, without hitting AGI thresholds: Consider a donor with AGI of $500,000 in 2020 (Display). She mapped out an action plan to maximize her deduction while giving to charities today and down the road. First, she immediately supported local COVID-19 relief efforts with a $350,000 cash gift to a public charity. She then planned to deploy the second round of donations from her DAF, which she funded earlier this year with long-term appreciated stock. By taking advantage of the temporary tax benefits under the CARES Act, she receives a combined deduction of 100% of AGI—thus reducing her income taxes—while quickly disbursing funds to preferred causes at a time of heightened need.

- Couple charitable gifts with income-generating strategies: 2020’s unique circumstances also present unusual planning opportunities. For example, donors who have stock options may be able to exercise those options, make a gift to charity, and take a deduction in the amount of the gift up to 100% of AGI.

At the other end of the spectrum, many Americans will have lower taxable income this year due to the pandemic, along with a lower effective tax rate—a situation ripe for a Roth IRA conversion. When combined with the CARES Act repeal of the AGI limitation on cash gifts to public charities, donors making a large enough donation could convert a portion of their traditional retirement account to a Roth tax-free.

- Use a QCD to offset income tax: The qualified charitable distribution (QCD) allows individuals over 70½ to annually donate up to $100,000 in IRA assets directly to charity*** while excluding the amount donated from taxable income. Many donors utilize a QCD to make a charitable gift to offset all or part of the taxable income from their required minimum distributions (RMDs).

While the CARES Act did not alter the QCD rules, it waives RMDs for 2020. Should you make a gift via the QCD if you are not taking your RMD? It depends. If you plan to itemize deductions in 2020, a gift from non-IRA assets may be preferable, especially if you’re able to donate highly appreciated securities. However, if you aren’t likely to itemize in 2020, a QCD may be a good alternative. Though the gift will not reduce your taxable income, donating pre-tax assets tax-free lowers your IRA balance, which could reduce future RMDs.

Though the clock is ticking on these CARES Act incentives, donors shouldn’t reflexively rush in. It’s essential to weigh the benefits against the tax incentives from other giving strategies. For example, you may be better off making donations from non-IRA assets—especially when gifting appreciated securities (to avoid capital gains tax exposure)—thereby preserving the IRA’s tax-deferral benefits.

Could Tax Law Changes Play a Role?

Amid ongoing uncertainty surrounding control of the Senate, it’s hard to gauge how much of President-Elect Biden’s agenda will become law, including his tax proposals. If his plans gain traction in Congress, the attractiveness of charitable giving could change for different cohorts. For example, one proposal raises the top marginal long-term capital gains rate from 23.8% to 43.4% (inclusive of the 3.8% Medicare surcharge) for taxpayers with income above $1 million. Such a change would make donating appreciated securities and avoiding capital gains more compelling for very high earners.

At the same time, Biden’s campaign proposed capping the value of itemized deductions at 28% for those earning more than $400,000. Taxpayers earning above that income threshold with tax rates higher than 28% would face limited itemized deductions, including the charitable income-tax deduction. This change would reduce the value of the deduction for high earners.

On balance, the tax advantages associated with charitable giving—and the relative advantage of giving different types of assets—may evolve. Donors should focus first on how and where they want to give, then work with professional advisors to determine which assets to give and how the timing might optimize their overall tax picture.

Doing Your Part

As you’re doing your part to make a difference, make sure that you’re maximizing the benefits– both for you and your cherished cause. While the election results create some uncertainty, we do know that the CARES Act incentives are compelling. Before they expire on December 31, talk to your tax professional about your giving strategy and keep lending the hand that the world so desperately needs.

- Jennifer Ostberg, CFP®, CAP®

- Director—Personal Philanthropy Services

* The $300 deduction for individuals who do not itemize their deductions will remain beyond 2020. This should increase donations from individuals who otherwise may not choose to make a charitable contribution. Cash donations to donor-advised funds (DAFs) or supporting organizations do not apply.

** Existing carryover rules still apply.

***Sponsoring organizations with donor-advised fund programs are not qualifying charities for QCDs.