The COVID-19 pandemic, together with its associated policy response, has already shattered historical records. The plunge in global GDP and the blowout in government deficits witnessed through the first half of 2020 are unprecedented outside of wartime.

But the story isn’t over. The pandemic is likely to have longer-running repercussions of historical scale, too—not only for societies, but for economic performance and government policies. It’s difficult to predict the precise shape of those repercussions, but homing in on areas where the pandemic’s impact is reinforcing existing long-term trends—pushing on an open door, if you like—should be a major focus.

In our view, deglobalization, a continuing trend toward populist politics and the consequences of mounting government debt are three key themes to pursue.

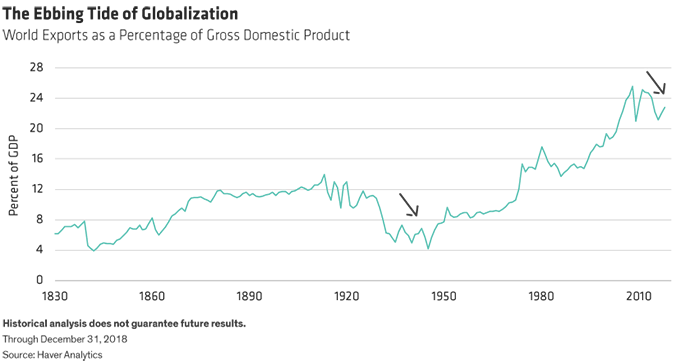

Have We Passed Peak Globalization?

Take the first of those themes—deglobalization. Over the last 30 years, the world has seen an era of unparalleled international economic cooperation and integration—with China at the heart of the process.

As trade boomed, exports rose steadily as a percentage of gross domestic product (GDP) (Display). Following the global financial crisis (GFC), this trend started to reverse. This was partly a result of vulnerabilities revealed by the GFC, but an increase in onshoring of production—driven by automation—also had an impact.

More recently, high-profile trade wars have shaken the institutional framework for free trade, with the global rise of populism stoking the frequency and intensity of trade disputes. Public policies are becoming more national and less global—a channel for populism that we call “raising the drawbridge.” In addition to one-on-one country disputes, we’ve also seen withdrawals from multinational arrangements, such as the Trans-Pacific Partnership and the Paris Climate Accord. The anti-Brussels sentiment that led to Brexit is another notable example of populist-inspired deglobalization momentum.

COVID-19 amplifies some of the causes of the upswing in populist politics. It has revealed yet another downside of global connectedness—efficient transmission of viruses.

Many of the cohorts in society who were already the losers from 30 years of globalization and market-based policies—minorities, lower-skilled workers and young people—have been hit hardest in this crisis. In some countries, far from drawing people together, the pandemic has highlighted societal fractures, institutional failures and other weaknesses. In short, populist pressures are intensifying—and, with them, more downward pressure on globalization.

A material decline in international trade integration would be a major structural shift for the world economy. Globalization has been a powerful positive supply shock, boosting economic growth and productivity while damping down inflation. We should expect the opposite effect as this process reverses. To stretch the metaphor, if COVID-19 opens the deglobalization door even further, the escalating geopolitical conflict between China and the West in the wake of the pandemic threatens to blow it off its hinges.

The ongoing trade war between China and the US is one of the most obvious signs that the mutually beneficial period of global cooperation is over. But the rising tension is about far more than trade. It’s about a tectonic shift in the global balance of power, with China and India emerging from a long slumber and the West, while remaining important, slowly losing power and influence.

Government Debt Overhang and Financial Repression

These developments clearly intensify the global challenges of policymaking. But there are domestic challenges, too. Here, perhaps the most important area in which COVID-19 is pushing on an open door is rising government debt (Display). Public-sector debt in developed economies had already reached record highs before the pandemic emerged, with gross government debt well over 100% of GDP for the G-7 nations. The massive fiscal support unleashed this year could lift the debt ratio by 20% or more for many countries.

How governments choose to deal with the debt overhang will go a long way toward determining the secular outlook. Historically, there have been a number of choices: default, growth, austerity and financial repression, but not all are on the menu this time around.

It would be problematic—delusional, perhaps—to rely on strong economic growth, given the unfavorable demographic trends and subdued prospects for productivity growth. Populism’s resurgence will likely further reduce the appetite for a long fiscal austerity effort, with higher taxes and spending cuts. Outright default is another option, but reneging on domestic-currency debt would be a politically fraught decision—and a historical anomaly.

What has been more historically common—for example, in the aftermath of World War II—is financial repression. Many countries during this era used a mixture of ultralow interest rates and modest inflation to reduce debt-to-GDP ratios. Japan has used similar policies over the past decade to stabilize its public debt at just under 240% of GDP (and much lower if we exclude government debt on central bank balance sheets). Low interest rates and modest levels of inflation have been powerful tools in the past—and could be again.

Indeed, evidence of a shift to that approach continues to accumulate. One side of the equation is already in place. The level of interest rates is extraordinarily low, with policy rates now set at or below the zero lower bound. In addition, the structure of nominal government bond yields is now heavily controlled, courtesy of successive rounds of quantitative easing and yield-curve-control frameworks.

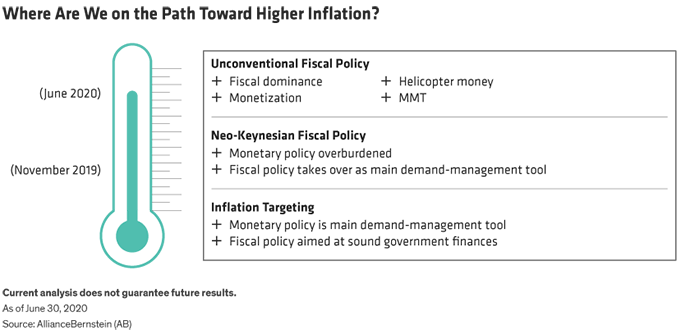

Is Higher Inflation Achievable? Regime Change Is the Key

The missing piece is, of course, inflation, which seems a long way away today. For the time being, COVID-19 and the economic dislocations it has created pose a challenge to our longer-term view of higher inflation. Developed economies are operating well below their economic potential today, and that could continue for some time—leaving huge output gaps.

But our longer-term inflation view isn’t dependent on cyclical factors or the immediate disruptive effects of the pandemic on pricing behavior. Rather, it’s all about changes in the global monetary and fiscal policy regime, driven in turn by the debt overhang, populism and deglobalization. And as we’ve discussed, these trends are being reinforced by the changes the pandemic has ushered in. In fact, COVID-19 has already seen widespread acceptance of two factors needed for a higher-inflation regime.

The first is recognizing the necessity for central banks to finance fiscal stimulus—monetary and fiscal policy working in concert or joined at the hip. The second factor is the idea that money should be channeled into the real economy—not into banks. Pushing funds into the real economy is much more likely to raise consumer prices, in contrast to the post-GFC experience when funneling money into banks drove up asset prices instead.

But there’s one more ingredient needed to give inflation a chance to ignite, and it’s in the hands of central banks. It involves taking further steps into unconventional policy territory (Display). In order to generate sustained higher inflation rates, central banks need to reset inflation expectations higher.

This will require a credible commitment—just as it did (in reverse) in the early 1980s, when central banks worked to break the back of rampant high inflation. Today, a commitment to breaking convention is likely to involve central banks downgrading or even abandoning their inflation targets. These targets, aided by demographics and globalization, have underpinned the low-inflation era of the last three or four decades. To reverse the tide, policymakers will need to undermine the credibility of the current monetary-policy regime.

We’ve seen baby steps. In August, the US Federal Reserve announced a major change in its policy framework to “average inflation targeting.” Moving forward, the Fed will be more willing to let inflation run above the established 2% target before it considers hiking interest rates. But while this is a welcome move, it’s unlikely to be enough by itself to generate a material shift higher in inflation performance.

As it stands, the Fed’s new framework is still rooted in the old policy regime, for fear that a bolder move would lead to a market overreaction. But it’s just that type of overreaction that central banks need to risk if they want to jolt markets and shift inflation expectations higher.

Have Expectations Already Started to Budge?

As we mentioned, several of the key pieces for a higher-inflation environment are falling into place. With central banks now openly toying with their policy frameworks and with money-financed fiscal stimulus now commonplace, we’re certainly closer now than we were a few months ago.

It may seem odd to talk about the chances of higher inflation during a massive slump in global activity, but a couple of recent developments suggest that the topic is at least worth a discussion. Consumer prices jumped sharply in June and July across the globe, and that looks to have continued into August in some countries. We’ve also seen an upward shift in some market-based measures of expected inflation.

The CPI jump is likely more noise than signal, but it’s broad-based. At a time when the cyclical inflation story is a tug-of-war between deficient demand and impaired supply, that noise shouldn’t be ignored. When we add policy regime shift into the mix—a willingness and an ability to accommodate higher inflation—the stakes become even higher.

Are inflation expectations breaking loose? Right now, changes in breakeven inflation rates in the market for Treasury Inflation Protection Securities (TIPS) seem driven more by liquidity considerations. We are starting to see some signs of inflation uncertainty—in the form of a wider distribution of expected inflation outcomes—in survey data. It’s a tentative development, but is worth watching.

So, getting back to our question of inflation and when the narrative will shift, our answer for now seems to be not quite. But we’ve started on that path, and, with markets still priced for Japanese-style deflation, that’s an important development.

- Darren Williams

- Director—Global Economic Research

- Guy Bruten

- Chief Economist—Asia-Pacific ex China

Darren Williams is Director—Global Economic Research at AllianceBernstein (AB). Guy Bruten is Chief Economist—Asia-Pacific ex China at AB.