Rumblings about potential tax code changes have caught investors’ attention as all eyes focus on the legislative twists and turns unfolding in DC. And amid widespread media coverage, headlines trumpeting a possible doubling of the top long-term capital gains rate—from 23.8% to 43.4%—certainly stand out. To make matters worse, the change may take effect retroactively, leaving taxpayers little to no wiggle room to plan ahead.

Some investors have already thrown in the towel, resigning themselves to unwelcome news and heightened uncertainty. But don’t be tempted to disengage. There are concrete steps you can take right now to invest in a more tax-efficient manner.

Button Up Your Portfolio

First, make sure your portfolio is appropriately positioned for after-tax success in the current tax rate environment:

Look Through a Tax Lens: Keep taxes in mind when evaluating strategies. While pretax returns might confer bragging rights, it’s their after-tax counterparts that matter most for taxable investors. Tax-inefficient investments should only be held in taxable accounts when diversification and/or return enhancement benefits outweigh incremental tax costs. Lean into tax-efficient strategies (including passive ETFs, index-driven strategies, and tax-aware active strategies) in accounts that are taxable.

Search Out Synergies: Beyond investing in tax-efficient strategies, explore complements to existing investments that will improve the tax efficiency of your allocation as a whole. Passive ETFs and mutual funds may be tax efficient on their own, but they don’t play as nicely in the sandbox with others. To put it plainly, their tax savings do nothing for other active strategies in an allocation. In contrast, an index-driven, tax-loss-harvesting strategy is designed to capture synergies, improving the after-tax returns for a diversified asset allocation overall.

Locate Assets Logically: For many investors, a balanced allocation will include some exposure to tax-inefficient strategies—like hedge funds—which tend to generate returns that are taxed as ordinary income and/or short-term capital gains. While valuable in the context of an overall allocation, they are not necessarily appropriate in taxable accounts. Instead, house such investments in tax-deferred accounts (401(k), IRA, cash balance plans, etc.). Some investors will not have enough tax-deferred capacity to hold all the tax-inefficient strategies they want to own. In that case, it may be possible to increase tax-deferred investing capacity by allocating to alternative tax-deferred strategies offered by the life insurance industry, like private placement annuities and life insurance. Investors should work with their advisors to evaluate the cost and tax benefit of allocating more to these vehicles.

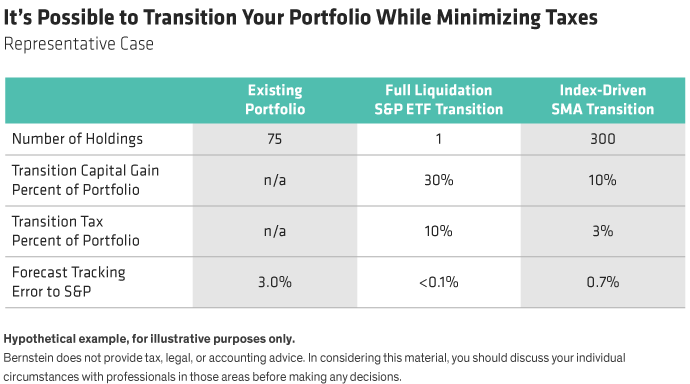

Try a Tax-Savvy Transition

Building a tax-efficient allocation from scratch might seem easy but transitioning current investments to a more “buttoned-up” tax profile may prove both difficult and expensive!

That’s because moving to an ETF or mutual fund likely involves selling every current holding, and simultaneously realizing all unrealized gains. Fortunately, there’s another way. You can significantly reduce the gains realized by transitioning existing investments to a tax-efficient strategy within a Separately Managed Account (SMA). Using this approach, many positions can be maintained—thereby deferring potential capital gains.

Take Pam, an investor looking to effectively position her portfolio in advance of looming tax hikes. She wants to migrate her 75-position stock portfolio to a tax-efficient, S&P tracking strategy. Pam is considering a move to a tax-efficient S&P ETF where future gains can be deferred indefinitely, until she sells the positions. She also hopes to find some relief from paying ongoing capital gains tax due to turnover in her current actively managed portfolio. Unfortunately, since ETFs must be purchased with cash, the only way to move from her current strategy is to sell out of all her existing holdings, which would create a 30% capital gain and at least a 10%1 capital gains tax hit!

With careful analysis, Pam can choose from a range of options that strike a balance between conforming to her ultimate allocation while maximizing after-tax returns and deferring unrealized gains.

For instance, instead of selling out of all her existing positions, she can build around them, moving to an index-driven SMA strategy and increasing the number of holdings to as many as 300. This approach gets Pam to her desired outcome—a tax-efficient portfolio, with considerably fewer capital gains and associated taxes, at 10% and 3%, respectively. Notably, the path of returns in Pam’s new portfolio will be roughly similar to what she’d experience with an S&P ETF, which aims to mirror the performance of the broad market. She’ll also enjoy similar tax efficiency with no capital gains taxes unless she sells.

Should You Make a Preemptive Move?

So far, we have discussed strategies for reducing gain realization. But some investors might wonder, “Could accelerating gain recognition before capital gains tax rates increase produce better after-tax outcomes?” It’s a risky proposition. Proposed tax legislation may not make it to the floor until later this year—and keep in mind, not everyone will be affected. Plus, the effective date of new tax rules remains a moving target.

The bottom line is that we don’t recommend going down that road right now. For most investors, it does not make sense to accelerate capital gains taxes for an uncertain benefit (potentially getting out in front of higher tax rates later)—especially when the chance to act upon more concrete information may emerge down the road. We’ve thought through the math to determine whether proactive gain realization makes sense—at a high level, it involves weighing the difference in tax rates (today vs. future rates), expected returns, and intended holding period. When costs (including current tax expenses) and benefits are uncertain, you are even more incentivized to wait for more information. Ultimately, due to possible retroactive application of any eventual law, the rate may have already gone up even as you’re reading this now (negating any attempt to act in advance).

On the other hand, investors and advisors should monitor tax legislation. And be on the lookout for two distinct scenarios where it may make sense to forge ahead:

- If an investor can improve the after-tax return potential of her allocation with reasonable current tax costs, she needn’t wait for clarity on tax changes to do so (like Pam above).

- If it becomes clear that tax rate increases will be implemented for next year, investors (particularly those with concentrated positions) may be incentivized to implement changes, including those that generate significant gains, before the end of 2021.

Investors should start having discussions today about what they will do if they have a chance to make changes before a tax increase takes effect. This will ensure they have a plan in place to move decisively and with more clarity.

Make an Informed Decision

The first step to improvement is assessment. Ask your advisor to ensure your portfolio is positioned for after-tax success. Many investors can improve their portfolio’s tax efficiency at a reasonable tax cost. Work with your advisor to determine what changes you will make even if your tax rates don’t change. Then develop a strategy for additional changes assuming you have an opportunity to act before any new legislation takes effect.

- John McLaughlin

- Portfolio Manager—Tax-Managed Strategies and Transitions

- Paul Robertson

- CIO, Tax-Managed Strategies—Equities

1 Based on tax legislation in place at the beginning of 2021.