Despite turbulence in early 2020, the market for Initial Public Offerings (IPOs) didn’t skip a beat. The $156 billion raised on US exchanges during the year exceeded the previous three years combined.1 Plus, companies took advantage of new ways to tap public markets—including direct listings and SPACs, which represented around 50% of IPO volume in 2020.2

For early shareholders, an IPO can lead to tremendous wealth. Google, for example, rose 18% on its first day of trading back in 2004. And it’s not alone. Since 1990, companies that have gone public have averaged a comparable first-day bump of 18.8%.3 Many haven’t stopped there. For instance, Google has gone on to reward shareholders with returns averaging 25.5% per year through 2020.

Yet while headlines often tout the big IPO winners, not all companies enjoy instant success. In recent decades, the average first-day uptick for companies going public has dwindled as firms delay their public debut and increase their initial offer size (in $). In the 1990s, stock prices climbed an average of 24% from the initial offer price on day one, whereas US IPO investors gained half of that on average in the 2010s.

IPO Stocks Are More Volatile

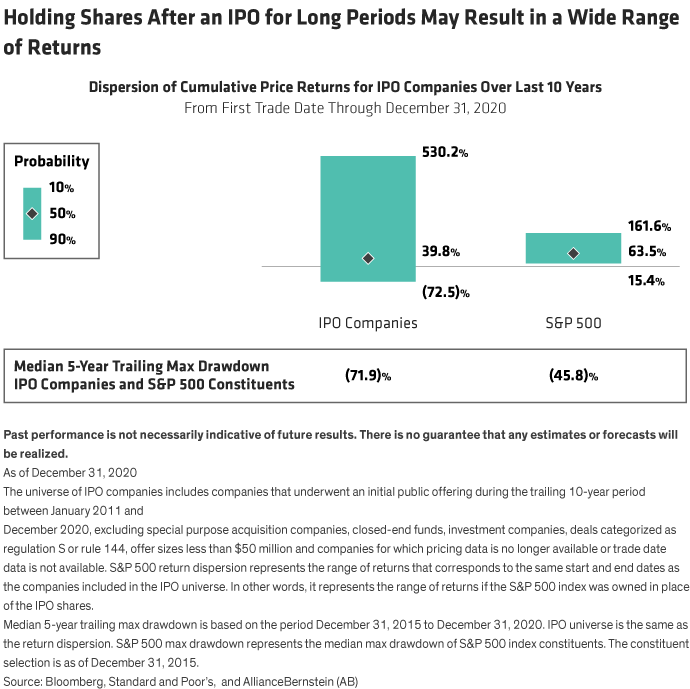

IPOs offer the potential for a windfall, but investors must be prepared to withstand the uncertainty. We compared the returns of a representative universe of companies that underwent a traditional Initial Public Offering in the last 10 years4 to the returns of their counterparts in the S&P 500 stock index over the same periods (using the first trade date of each IPO stock through December 31, 2020). The range of returns for the IPO universe varied widely, with the median cumulative price performance reaching 39.8% (Display). By comparison, investors could expect a much smaller dispersion of returns from investing in the S&P 500—and at 63.5%, the median cumulative return was nearly one third higher.

Then there’s risk. To gauge the downside, we also compared the max drawdowns of the representative universe of IPO stocks to all companies in the S&P 500 during the last five years. The (72%) median drawdown for IPO stocks eclipsed the (46%) median drawdown of S&P 500 constituents. Interestingly, the single largest drawdown in the S&P 500 Index was only (33.8)%. This underscores the inherent risk of too much exposure to any single stock, especially for investors in a newly listed company relative to owners of mature, large-cap holdings.

Clearly, the stakes are high for founders, investors, and employees of pre-IPO companies. Decisions made before and after the IPO may ultimately mean the difference between success and failure in meeting investors’ goals. Fortunately, thoughtful planning can help pre-IPO shareholders tilt the odds in their favor. Bernstein can help answer the critical questions that arise all along the IPO timeline.

Before the IPO:

How much core capital will I need to secure my financial future?

- Quantifying the nest egg you’ll need to ensure financial independence can set a target for future diversification while dimensioning capacity for pre-IPO legacy planning.

Which estate planning moves should I consider in the run-up to the IPO?

- Transferring shares for your heirs to GRATs or other trusts can take advantage of pre-IPO valuations and significantly reduce estate taxes down the road.

- Shareholders face critical decisions about how much to fund into GRATs and should stress-test different offering prices to gauge the impact, both now and for future generations.

Should I exercise my employee stock options early?

- Exercising stock options after a successful IPO can trigger hefty taxes. Option holders who proactively exercise at lower valuations may meaningfully reduce their tax obligations.

- When weighing the trade-offs, option holders must consider the type of options, whether the stock qualifies for QSBS,5 costs of exercising, and their own liquidity position.

What if I need liquidity before the IPO?

- There is a growing secondary market for private company shares, and matching websites can connect buyers with sellers.

- Before proceeding, shareholders should weigh price discounts and commission charges.

After the Underwriter’s Lock-Up Expires (Usually 180 Days After the IPO):

How do I manage single-stock exposure?

- Shareholders should devise a diversification plan detailing appropriate share amounts and timing, outlining which shares or options to divest first.

What about restrictions and blackouts?

- Shareholders and employees are typically subject to a lock-up agreement that prevents selling for six months. And even when the lock-up expires, insiders can only trade during certain windows.

- To address these constraints, many turn to a 10b5-1 plan—a prearranged, written selling plan that facilitates the sale of company stock over time despite blackout trading dates.

How can I help the charities I care about?

- Donate highly appreciated stock in-kind, generally after the IPO. A donor-advised fund can provide a charitable deduction to reduce tax in a year with a large capital gain.

Navigating the pathway to liquidity can be tricky—and for most, it will be the single most consequential financial event of their lifetime. By working with your financial advisor, you can make sure some of your windfall doesn’t wind up lost in transition.

- Christopher Clarkson

- National Director, Planning | Foundation & Institutional Advisory

- Alex Coulard

- Investment Analyst—Bernstein Private Wealth Management

1Funds raised through primary share offerings only. Source: Bloomberg.

2A Special Purpose Acquisition Company (SPAC) is a public shell company that raises money in an IPO in order to merge with a private operating company, allowing the target to become publicly traded. Source: AllianceBernstein and Bloomberg.

3Average first-day return represents the offer-size-weighted average of the returns for all US companies that underwent an initial public offering during the respective decade. Decade start and end dates are as of December 31. The analysis excludes special purpose acquisition companies, closed-end funds, investment companies, and deals categorized as Regulation S or Rule 144. Source: Bloomberg and AB.

4The universe of IPO companies includes all companies that underwent an initial public offering during the trailing 10-year period between January 2011 and December 2020, excluding special purpose acquisition companies, closed-end funds, investment companies, and deals categorized as Regulation S or Rule 144.

5According to IRC Section 1202, shareholders of Qualified Small Business Stock (QSBS) may exclude between 50%–100% of eligible gain from federal income taxation up to the greater of $10 million or 10 times the adjusted basis upon the sale.